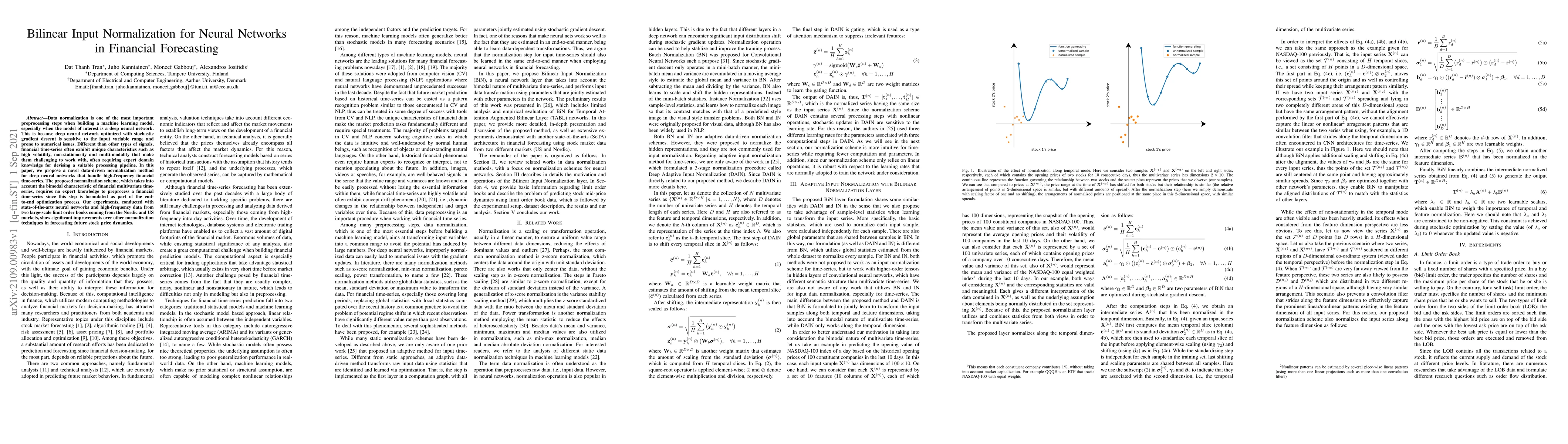

Data normalization is one of the most important preprocessing steps when

building a machine learning model, especially when the model of interest is a

deep neural network. This is because deep neural network optimized with

stochastic gradient descent is sensitive to the input variable range and prone

to numerical issues. Different than other types of signals, financial

time-series often exhibit unique characteristics such as high volatility,

non-stationarity and multi-modality that make them challenging to work with,

often requiring expert domain knowledge for devising a suitable processing

pipeline. In this paper, we propose a novel data-driven normalization method

for deep neural networks that handle high-frequency financial time-series. The

proposed normalization scheme, which takes into account the bimodal

characteristic of financial multivariate time-series, requires no expert

knowledge to preprocess a financial time-series since this step is formulated

as part of the end-to-end optimization process. Our experiments, conducted with

state-of-the-arts neural networks and high-frequency data from two large-scale

limit order books coming from the Nordic and US markets, show significant

improvements over other normalization techniques in forecasting future stock

price dynamics.

Discussion 0