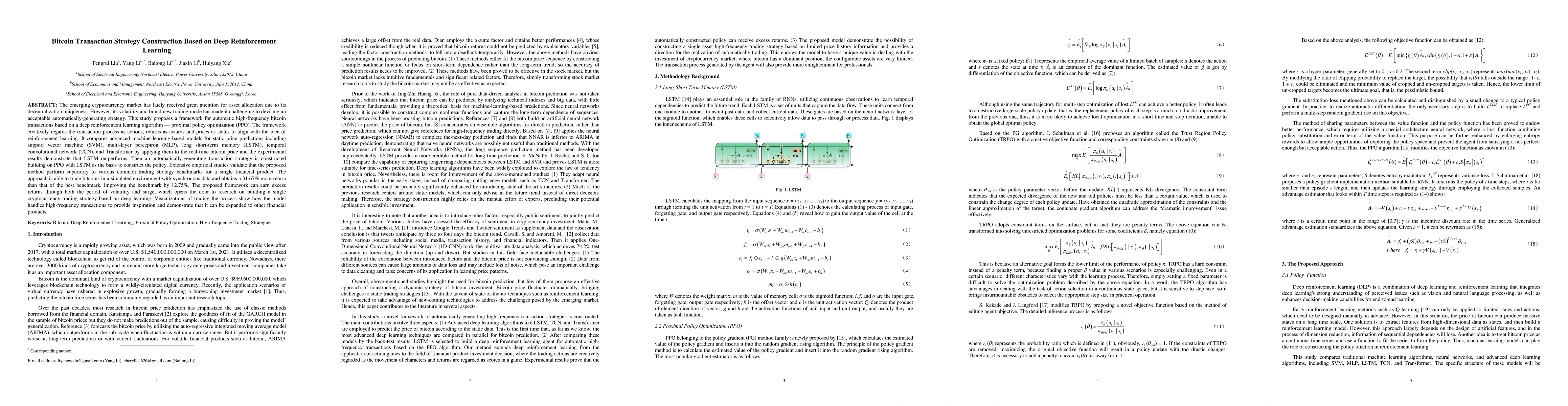

Bitcoin Transaction Strategy Construction Based on Deep Reinforcement Learning

Publication

Metrics

AI Quick Summary

This paper proposes a deep reinforcement learning framework using Proximal Policy Optimization (PPO) to construct an automatic high-frequency bitcoin transaction strategy. The study compares various machine learning models for price prediction, finding that LSTM outperforms others, and demonstrates that the proposed PPO-based strategy achieves superior performance, earning 31.67% more return than the best benchmark in a simulated environment.

Paper Preview

Abstract

The emerging cryptocurrency market has lately received great attention for asset allocation due to its decentralization uniqueness. However, its volatility and brand new trading mode have made it challenging to devising an acceptable automatically-generating strategy. This study proposes a framework for automatic high-frequency bitcoin transactions based on a deep reinforcement learning algorithm-proximal policy optimization (PPO). The framework creatively regards the transaction process as actions, returns as awards and prices as states to align with the idea of reinforcement learning. It compares advanced machine learning-based models for static price predictions including support vector machine (SVM), multi-layer perceptron (MLP), long short-term memory (LSTM), temporal convolutional network (TCN), and Transformer by applying them to the real-time bitcoin price and the experimental results demonstrate that LSTM outperforms. Then an automatically-generating transaction strategy is constructed building on PPO with LSTM as the basis to construct the policy. Extensive empirical studies validate that the proposed method performs superiorly to various common trading strategy benchmarks for a single financial product. The approach is able to trade bitcoins in a simulated environment with synchronous data and obtains a 31.67% more return than that of the best benchmark, improving the benchmark by 12.75%. The proposed framework can earn excess returns through both the period of volatility and surge, which opens the door to research on building a single cryptocurrency trading strategy based on deep learning. Visualizations of trading the process show how the model handles high-frequency transactions to provide inspiration and demonstrate that it can be expanded to other financial products.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0