Publication

Metrics

AI Quick Summary

This paper investigates the theoretical consistency of Mack's bootstrap for estimating reserve distributions in non-life insurance. It finds that while Mack's bootstrap accurately mimics process uncertainty, it fails to capture estimation uncertainty. An alternative Mack-type bootstrap is proposed to address this, which performs better in simulations.

Paper Preview

Abstract

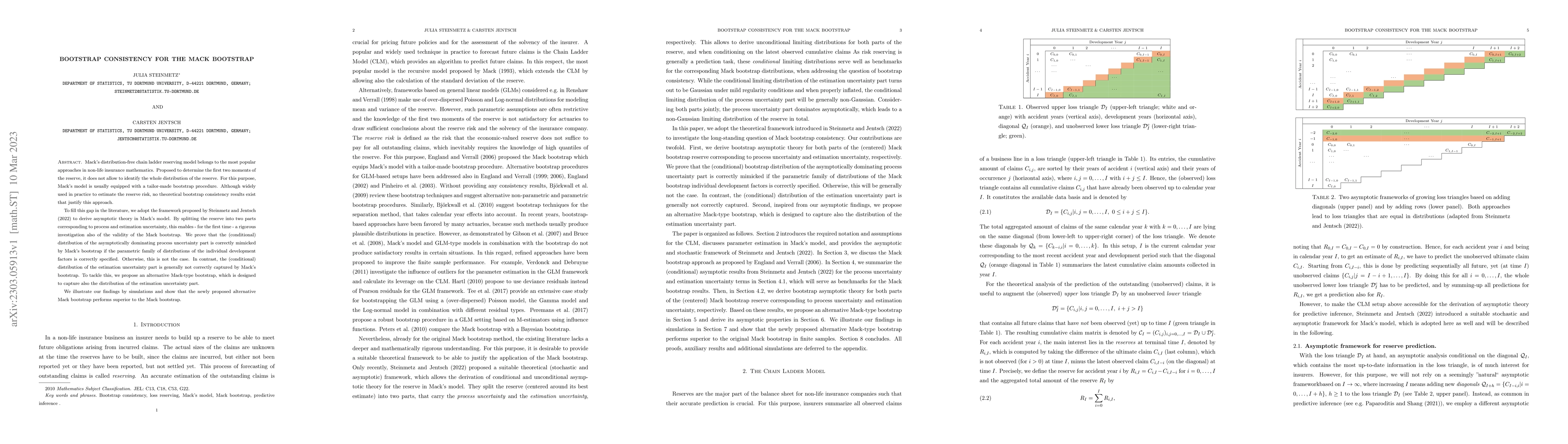

Mack's distribution-free chain ladder reserving model belongs to the most popular approaches in non-life insurance mathematics. Proposed to determine the first two moments of the reserve, it does not allow to identify the whole distribution of the reserve. For this purpose, Mack's model is usually equipped with a tailor-made bootstrap procedure. Although widely used in practice to estimate the reserve risk, no theoretical bootstrap consistency results exist that justify this approach. To fill this gap in the literature, we adopt the framework proposed by Steinmetz and Jentsch (2022) to derive asymptotic theory in Mack's model. By splitting the reserve into two parts corresponding to process and estimation uncertainty, this enables - for the first time - a rigorous investigation also of the validity of the Mack bootstrap. We prove that the (conditional) distribution of the asymptotically dominating process uncertainty part is correctly mimicked by Mack's bootstrap if the parametric family of distributions of the individual development factors is correctly specified. Otherwise, this is not the case. In contrast, the (conditional) distribution of the estimation uncertainty part is generally not correctly captured by Mack's bootstrap. To tackle this, we propose an alternative Mack-type bootstrap, which is designed to capture also the distribution of the estimation uncertainty part. We illustrate our findings by simulations and show that the newly proposed alternative Mack bootstrap performs superior to the Mack bootstrap.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0