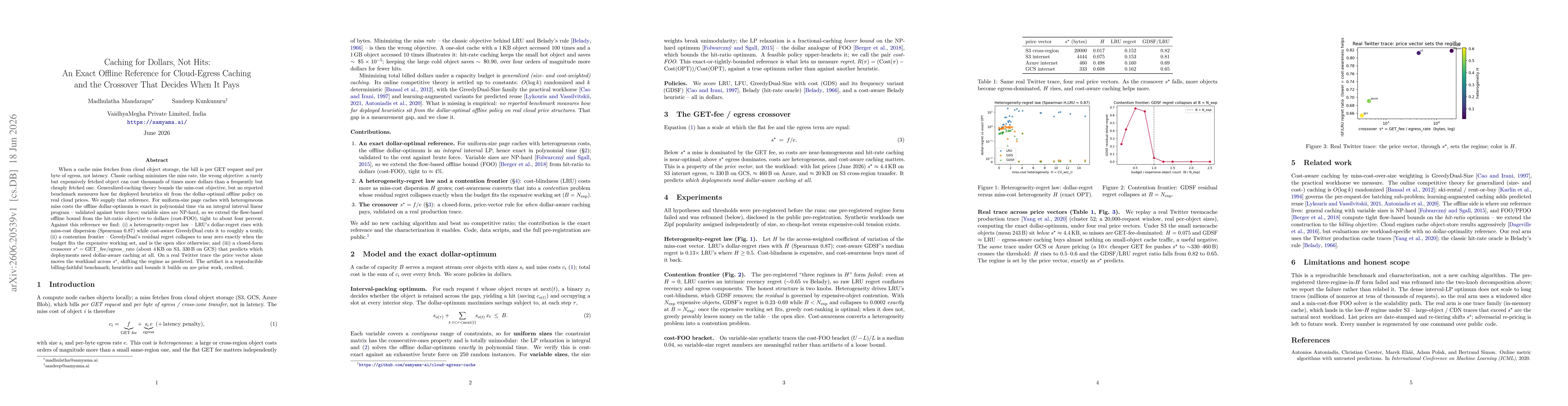

When a cache miss fetches from cloud object storage, the bill is per GET request and per byte of egress, not latency. Classic caching minimizes the miss rate, the wrong objective: a rarely but expensively fetched object can cost thousands of times more dollars than a frequently but cheaply fetched one. Generalized-caching theory bounds the miss-cost objective, but no reported benchmark measures how far deployed heuristics sit from the dollar-optimal offline policy on real cloud prices. We supply that reference. For uniform-size page caches with heterogeneous miss costs the offline dollar-optimum is exact in polynomial time via an integral interval linear program -- validated against brute force; variable sizes are NP-hard, so we extend the flow-based offline bound from the hit-ratio objective to dollars (cost-FOO), tight to about four percent. Against this reference we find: (i) a heterogeneity-regret law -- LRU's dollar-regret rises with miss-cost dispersion (Spearman 0.87) while cost-aware GreedyDual cuts it to roughly a tenth; (ii) a contention frontier -- GreedyDual's residual regret collapses to near zero exactly when the budget fits the expensive working set, and is the open slice otherwise; and (iii) a closed-form crossover s* = GET_fee/egress_rate (about 4 KB on S3, 330 B on GCS) that predicts which deployments need dollar-aware caching at all. On a real Twitter trace the price vector alone moves the workload across s*, shifting the regime as predicted. The artifact is a reproducible billing-faithful benchmark; heuristics and bounds it builds on are prior work, credited.

Discussion 0