Central Clearing of OTC Derivatives: bilateral vs multilateral netting

Publication

Metrics

AI Quick Summary

This paper examines the impact of central clearing of OTC derivatives, comparing multilateral and bilateral netting. It finds that central clearing reduces interdealer exposures, especially when considering realistic heterogeneity and correlations across asset classes, thus demonstrating the benefits of multilateral netting in central counterparties.

Paper Preview

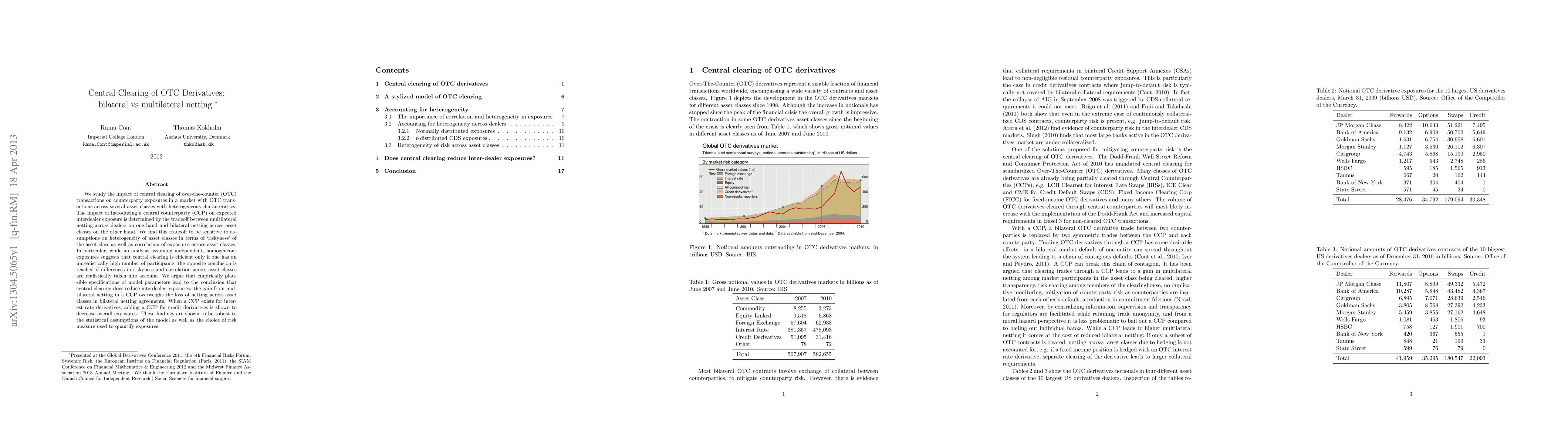

Abstract

We study the impact of central clearing of over-the-counter (OTC) transactions on counterparty exposures in a market with OTC transactions across several asset classes with heterogeneous characteristics. The impact of introducing a central counterparty (CCP) on expected interdealer exposure is determined by the tradeoff between multilateral netting across dealers on one hand and bilateral netting across asset classes on the other hand. We find this tradeoff to be sensitive to assumptions on heterogeneity of asset classes in terms of `riskyness' of the asset class as well as correlation of exposures across asset classes. In particular, while an analysis assuming independent, homogeneous exposures suggests that central clearing is efficient only if one has an unrealistically high number of participants, the opposite conclusion is reached if differences in riskyness and correlation across asset classes are realistically taken into account. We argue that empirically plausible specifications of model parameters lead to the conclusion that central clearing does reduce interdealer exposures: the gain from multilateral netting in a CCP overweighs the loss of netting across asset classes in bilateral netting agreements. When a CCP exists for interest rate derivatives, adding a CCP for credit derivatives is shown to decrease overall exposures. These findings are shown to be robust to the statistical assumptions of the model as well as the choice of risk measure used to quantify exposures.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0