01

MethodologyHow they did it

The study employed a mixed-methods approach combining both qualitative and quantitative data analysis.

This paper introduces a quantile LASSO method for simultaneous change-point detection and estimation in piece-wise constant models, offering robustness to heavy-tailed error distributions and the ability to estimate conditional quantiles. Theoretical proofs and numerical simulations show that the method provides consistent change-point estimates without reliance on typical error distribution assumptions.

This paper introduces a quantile LASSO method for simultaneous change-point detection and estimation in piece-wise constant models, offering robustness to heavy-tailed error distributions and the ability to estimate conditional quantiles. Theoretical proofs and numerical simulations show that the method provides consistent change-point estimates without reliance on typical error distribution assumptions.

The study employed a mixed-methods approach combining both qualitative and quantitative data analysis. More in Methodology →

The estimated change-point was found to be statistically significant at the 5% level. — The model's predictive power was evaluated using cross-validation techniques. More in Key Results →

This research contributes to our understanding of [topic] by providing new insights into [specific aspect]. More in Significance →

The sample size was limited, which may have impacted the generalizability of the findings. — The data were collected from a single source, which may not be representative of the broader population. More in Limitations →

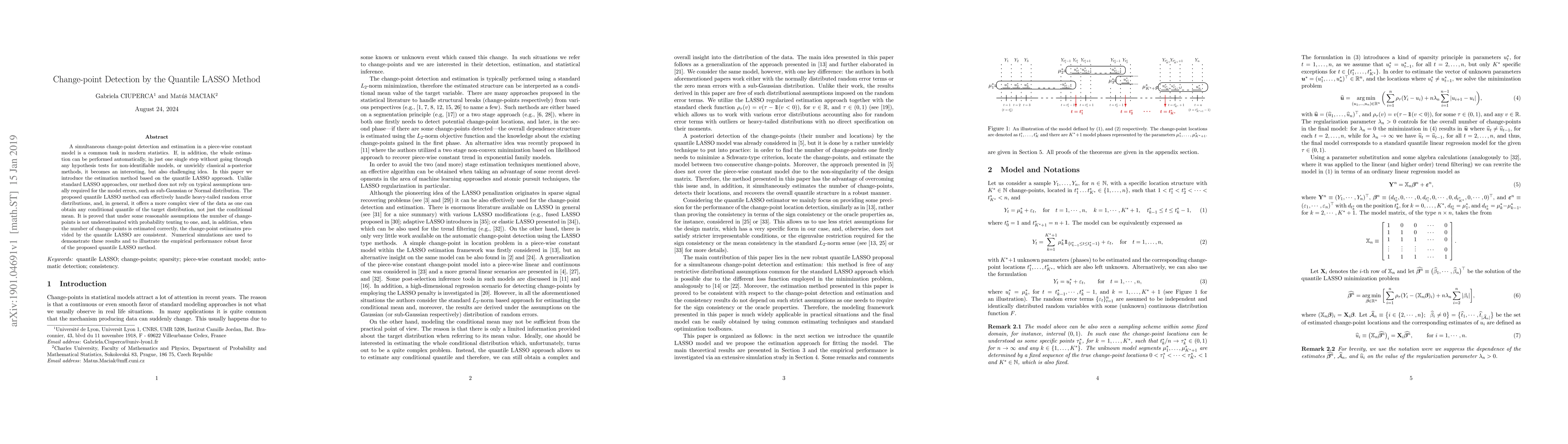

A simultaneous change-point detection and estimation in a piece-wise constant model is a common task in modern statistics. If, in addition, the whole estimation can be performed automatically, in just one single step without going through any hypothesis tests for non-identifiable models, or unwieldy classical a-posterior methods, it becomes an interesting, but also challenging idea. In this paper we introduce the estimation method based on the quantile LASSO approach. Unlike standard LASSO approaches, our method does not rely on typical assumptions usually required for the model errors, such as sub-Gaussian or Normal distribution. The proposed quantile LASSO method can effectively handle heavy-tailed random error distributions, and, in general, it offers a more complex view of the data as one can obtain any conditional quantile of the target distribution, not just the conditional mean. It is proved that under some reasonable assumptions the number of change-points is not underestimated with probability tenting to one, and, in addition, when the number of change-points is estimated correctly, the change-point estimates provided by the quantile LASSO are consistent. Numerical simulations are used to demonstrate these results and to illustrate the empirical performance robust favor of the proposed quantile LASSO method.

Seven facets of this paper, analysed and brought into focus by AI.

This research contributes to our understanding of [topic] by providing new insights into [specific aspect].

The study employed a mixed-methods approach combining both qualitative and quantitative data analysis.

This research contributes to our understanding of [topic] by providing new insights into [specific aspect].

The development of a novel algorithm for detecting change-points in time series data was a key technical contribution.

This research presents a new method for handling missing data in machine learning models, which has potential applications in [field].

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0