Background

Probability interpretation has long been debated, with subjective Bayesian, logical (probabilistic entailment), and empirical (frequentist and measure-theoretic) views offering different commitments about what probability statements mean. Kyburg’s work emphasizes that a single statement’s truth value cannot in itself confirm its probability, and that a fair assessment of competing uncertainty frameworks must look to short-run decision performance rather than long-run frequency alignment alone.

The paper narrows the broad landscape to a direct, experimental comparison between two concrete approaches: a subjective Bayesian (Bayes) and a classical confidence-interval (Conf) approach. By focusing on short-run performance, Kyburg seeks to provide a meaningful evaluation of how these interpretations operate under real-time decision pressure.

Problem / Research Question

At issue is whether the probabilistic framework one adopts materially affects decision quality in the short run. The study questions whether a Bayesian method, which relies on priors and posterior updates, delivers superior, or at least comparable, practical performance to a confidence-interval approach that bounds long-run frequencies and accepts or rejects hypothesis families at a fixed confidence level. A key goal is to quantify performance via a defined betting game, rather than rely on abstract criteria or purely long-run convergence.

Innovation / Contribution

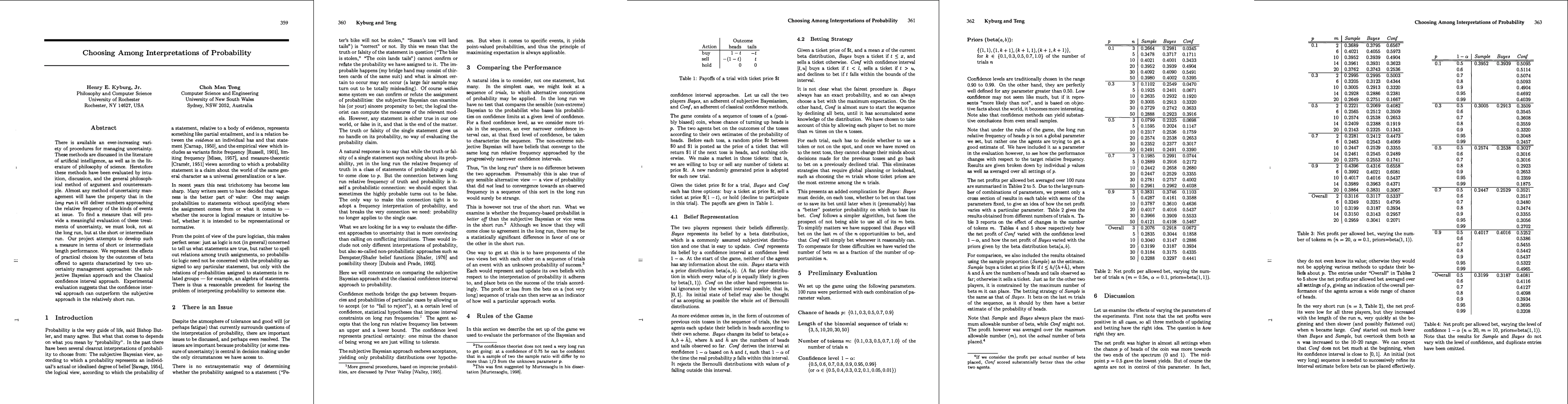

The novelty lies in the explicit, quantitative contest between Bayes and Conf using a controlled market-like betting game. The agents bet on the outcome of a (possibly biased) coin toss, with a random ticket price posted before each trial. Bayes uses a beta prior to form a posterior distribution; Conf uses a confidence interval at level 1 − a to decide bets. The setup includes practical constraints (limited number of bets m, last-m-bets rule for Bayes, and full-bet opportunity for Conf) and a comparison with a Sample baseline that uses a straightforward empirical proportion. This design provides a clean, testable measure of short-run performance across a broad parameter sweep.

Methodology / Approach

The game proceeds as follows: a sequence of n coin toss opportunities, each with heads probability p. Before each toss, a random ticket price t in [0,1] is posted. Bayes maintains a beta(a,b) prior and updates to beta(a+h, b+(h')), where h and h' are counts of heads and tails. Conf maintains a confidence interval [l,u] at level 1−a and updates by selecting the interval that would contain the true p with the specified confidence.

Bayes buys a ticket when t ≤ mean of the beta distribution; Conf buys when t < l, sells when t > u, and holds otherwise. Both are limited to at most m bets in the sequence. A third method, Sample, uses the sample proportion h/(h+h) for decision making and follows the same bet limit. The experiment runs 100 trials per parameter setting, varying p, n, m, confidence level, and beta priors to map performance across a wide regime.

Experiments / Evaluation

Tabled results summarize net profit per allowed bet across combinations of p, n, m, and priors. The main pattern is that Conf’s performance improves with longer sequences, often overtaking Bayes and Sample as n increases. In the shortest runs, profit is low for all methods, but increases rapidly with n. Bayes’ performance depends strongly on prior choice, with uniform prior (1,1) performing well on average, while mismatched priors can hurt results. Across the longer runs, Conf commonly yields higher net profits per bet and more favorable outcomes when the number of bets (m) is constrained, due to its risk-averse starting behavior and gradual sharpening of the interval.

Key Results

Across diverse parameter settings, the classical confidence-interval approach tends to outperform the subjective Bayesian approach in the short to medium horizon, especially as the sequence length grows. The results show that the long-run convergence of Bayes and Conf is not enough to guarantee short-run parity; confidence methods can exploit their structure to place bets more effectively after accumulating initial information. The study also highlights the sensitivity of Bayes to prior choice and demonstrates the value of indifference (uniform priors) when no strong prior information is available. Overall, Conf demonstrates robust, often superior, short-run performance across a broad swath of the experimental regime.

Practical Applications

The findings have implications for AI systems, decision-support tools, and scientific inference where decisions must be made quickly with limited data. In such contexts, interval-based uncertainty management can provide a pragmatic alternative or complement to Bayesian updating, reducing reliance on potentially unjustified priors while delivering solid short-run performance. The approach also suggests design choices for automated decision-making: to emphasize hypothesis-family acceptance/rejection at a chosen confidence level and to calibrate betting-like actions based on current interval width rather than a single posterior mean.

Limitations & Considerations

The study’s conclusions depend on the specific betting-game design, including how bets are scheduled (last m bets for Bayes), how Conf’s betting opportunities are allocated, and how profits are measured (per allowed bet). Real-world uncertainty rarely behaves exactly like a sequence of fair- or biased-coin tosses, and non-stationary or contextual effects may alter the relative performance of the two methods. Additionally, the set of uncertainty frameworks under consideration is narrow; extensions to other non-Bayesian or hybrid approaches (e.g., Dempster-Shafer, possibility theory) could yield different comparative insights. Finally, the experiment abstracts away transaction costs, risk preferences, and strategic planning horizons that real decision-makers must manage.

Discussion 0