Collaborative Optimization in Financial Data Mining Through Deep Learning and ResNeXt

Publication

Metrics

AI Quick Summary

This research presents a multi-task learning framework using ResNeXt to optimize feature extraction and collaboration in financial data mining, demonstrating superior performance in classification and regression tasks on S&P 500 data compared to conventional deep learning models.

Paper Preview

Abstract

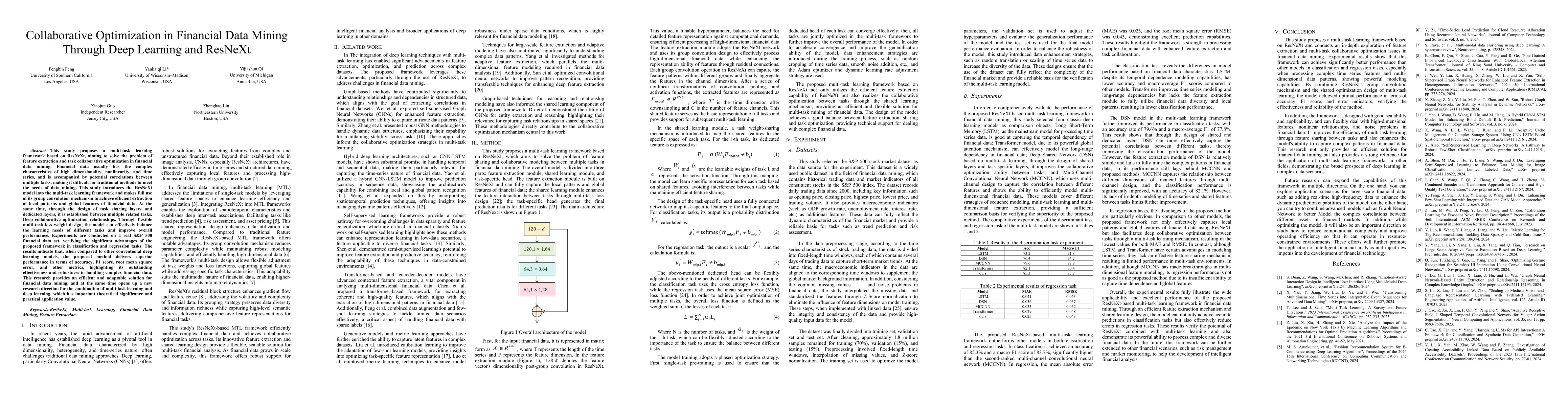

This study proposes a multi-task learning framework based on ResNeXt, aiming to solve the problem of feature extraction and task collaborative optimization in financial data mining. Financial data usually has the complex characteristics of high dimensionality, nonlinearity, and time series, and is accompanied by potential correlations between multiple tasks, making it difficult for traditional methods to meet the needs of data mining. This study introduces the ResNeXt model into the multi-task learning framework and makes full use of its group convolution mechanism to achieve efficient extraction of local patterns and global features of financial data. At the same time, through the design of task sharing layers and dedicated layers, it is established between multiple related tasks. Deep collaborative optimization relationships. Through flexible multi-task loss weight design, the model can effectively balance the learning needs of different tasks and improve overall performance. Experiments are conducted on a real S&P 500 financial data set, verifying the significant advantages of the proposed framework in classification and regression tasks. The results indicate that, when compared to other conventional deep learning models, the proposed method delivers superior performance in terms of accuracy, F1 score, root mean square error, and other metrics, highlighting its outstanding effectiveness and robustness in handling complex financial data. This research provides an efficient and adaptable solution for financial data mining, and at the same time opens up a new research direction for the combination of multi-task learning and deep learning, which has important theoretical significance and practical application value.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0