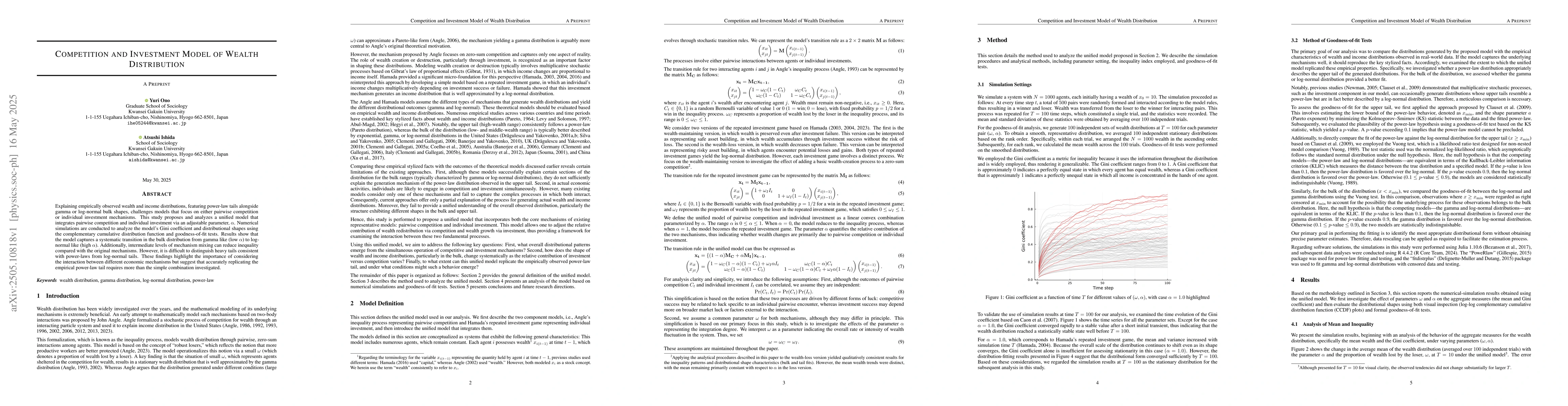

Explaining empirically observed wealth and income distributions, featuring

power-law tails alongside gamma or log-normal bulk shapes, challenges models

that focus on either pairwise competition or individual investment mechanisms.

This study proposes and analyzes a unified model that integrates pairwise

competition and individual investment via an adjustable parameter, $\alpha$.

Numerical simulations are conducted to analyze the model's Gini coefficient and

distributional shapes using the complementary cumulative distribution function

and goodness-of-fit tests. Results show that the model captures a systematic

transition in the bulk distribution from gamma like (low $\alpha$) to

log-normal like (high $\alpha$). Additionally, intermediate levels of mechanism

mixing can reduce inequality compared with the original mechanisms. However, it

is difficult to distinguish heavy tails consistent with power-laws from

log-normal tails. These findings highlight the importance of considering the

interaction between different economic mechanisms but suggest that accurately

replicating the empirical power-law tail requires more than the simple

combination investigated.

Discussion 0