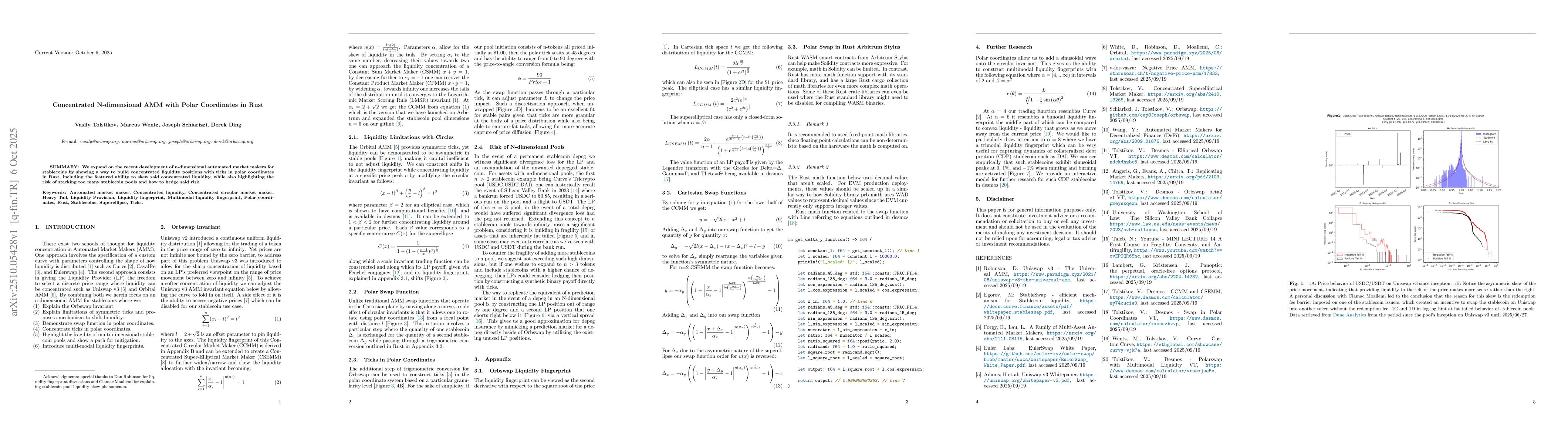

01

MethodologyHow they did it

The research employs polar coordinates to model concentrated liquidity positions in N-dimensional automated market makers (AMMs), using mathematical equations and empirical analysis of stablecoin pools on Uniswap v3. It integrates theoretical models with data from Dune Analytics and Desmos for visualization.

Discussion 0