01

MethodologyHow they did it

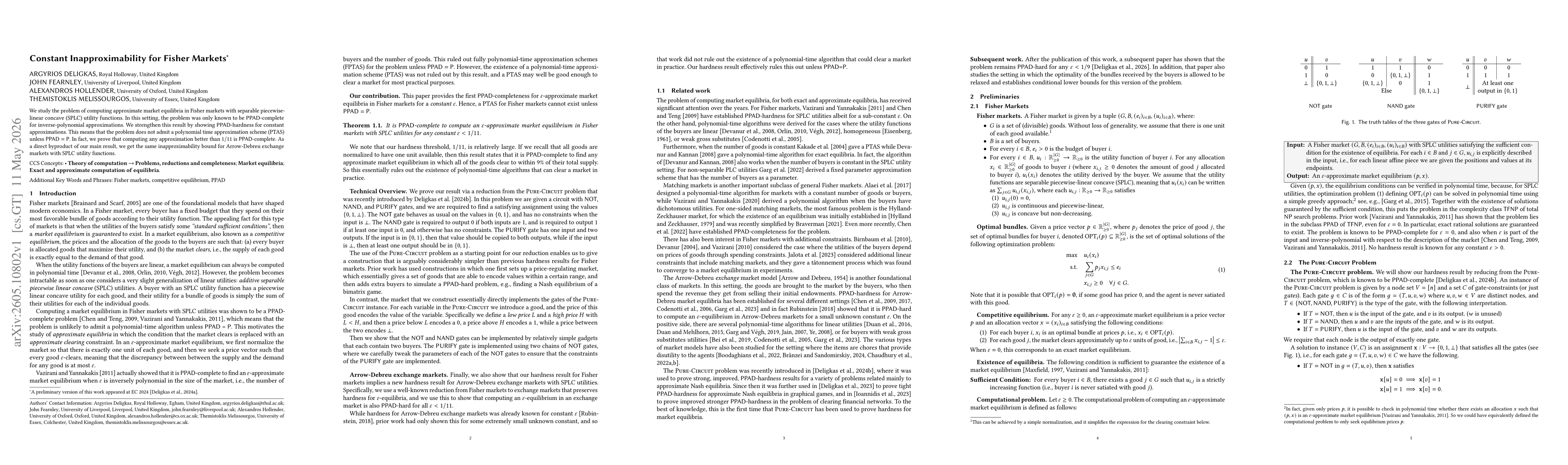

The authors provide a hardness reduction from the Pure-Circuit problem to Fisher markets with SPLC utilities, constructing gadget-based market instances where prices encode variable assignments. They define low and high prices to represent 0 and 1, respectively, and intermediate prices to encode the undefined value ⊥, then design price-regulating gadgets using buyers to simulate logical gates (NOT, NAND, PURIFY). The reduction extends to Arrow-Debreu exchanges via a standard preservation reduction of ε-equilibria hardness, establishing PPAD-hardness for constant ε.

Discussion 0