Constant versus Covariate Dependent Threshold in the Peaks-Over Threshold Method

Publication

Metrics

AI Quick Summary

This paper proposes a covariate dependent threshold based on expectiles for the Peaks-Over Threshold method, comparing it to constant and quantile regression thresholds in simulations and real data. The expectile threshold performs best for smaller to medium response values, while the constant threshold is superior for larger values.

Paper Preview

Abstract

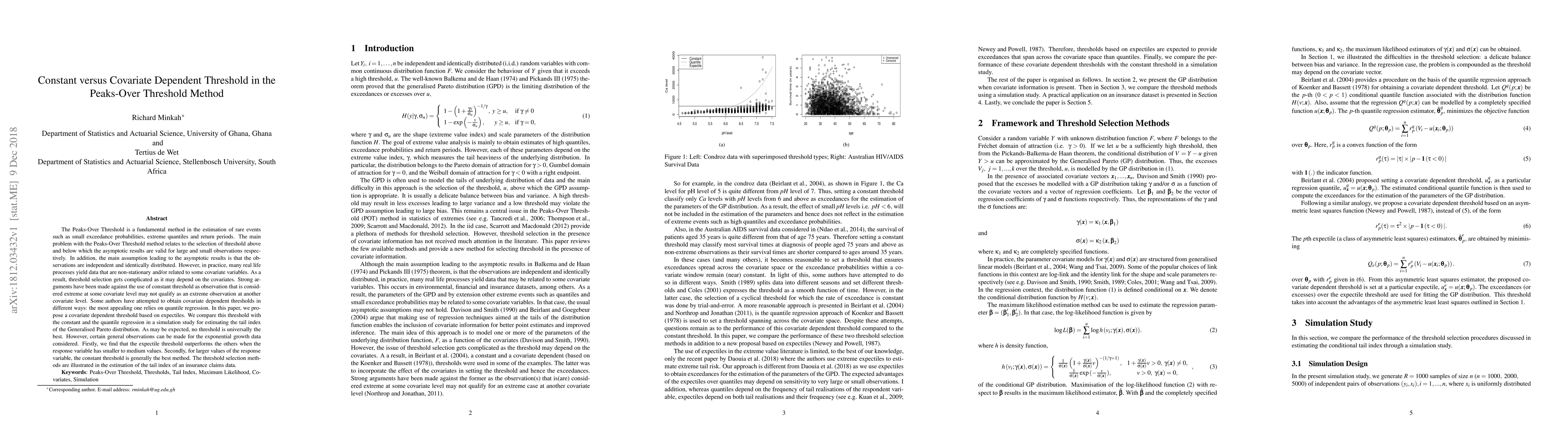

The Peaks-Over Threshold is a fundamental method in the estimation of rare events such as small exceedance probabilities, extreme quantiles and return periods. The main problem with the Peaks-Over Threshold method relates to the selection of threshold above and below which the asymptotic results are valid for large and small observations respectively. In addition, the main assumption leading to the asymptotic results is that the observations are independent and identically distributed. However, in practice, many real life processes yield data that are non-stationary and/or related to some covariate variables. As a result, threshold selection gets complicated as it may depend on the covariates. Strong arguments have been made against the use of constant threshold as observation that is considered extreme at some covariate level may not qualify as an extreme observation at another covariate level. Some authors have attempted to obtain covariate dependent thresholds in different ways: the most appealing one relies on quantile regression. In this paper, we propose a covariate dependent threshold based on expectiles. We compare this threshold with the constant and the quantile regression in a simulation study for estimating the tail index of the Generalised Pareto distribution. As may be expected, no threshold is universally the best. However, certain general observations can be made for the exponential growth data considered. Firstly, we find that the expectile threshold outperforms the others when the response variable has smaller to medium values. Secondly, for larger values of the response variable, the constant threshold is generally the best method. The threshold selection methods are illustrated in the estimation of the tail index of an insurance claims data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0