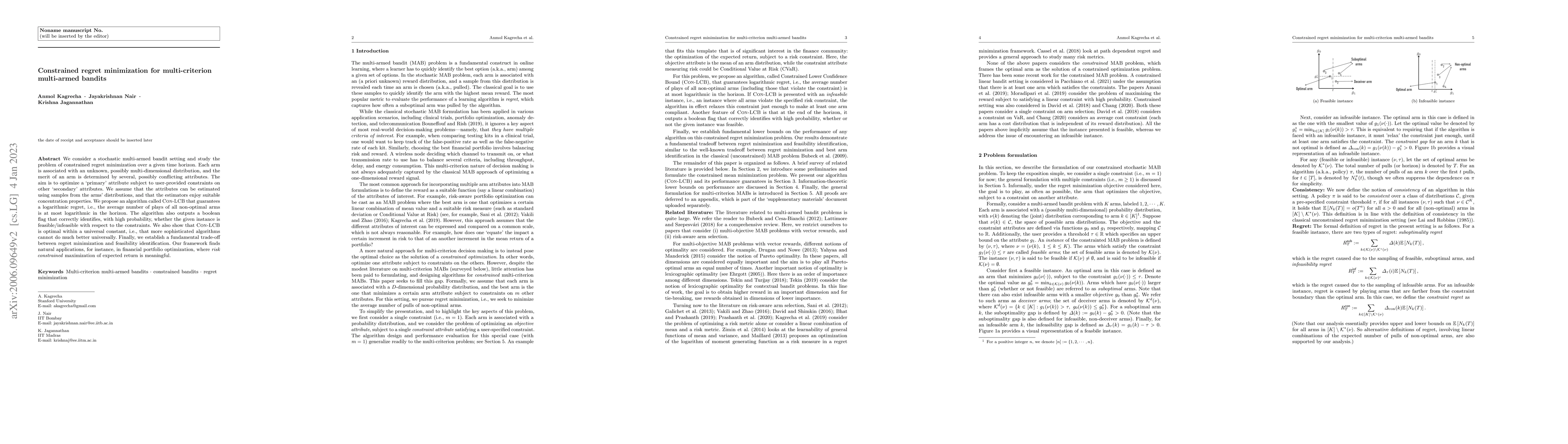

Constrained regret minimization for multi-criterion multi-armed bandits

Publication

Metrics

AI Quick Summary

This paper proposes a Con-LCB algorithm for constrained regret minimization in multi-criterion multi-armed bandits, achieving logarithmic regret and identifying feasibility with respect to secondary constraints. The algorithm's optimality and a fundamental trade-off between regret and feasibility are also demonstrated.

Paper Preview

Abstract

We consider a stochastic multi-armed bandit setting and study the problem of constrained regret minimization over a given time horizon. Each arm is associated with an unknown, possibly multi-dimensional distribution, and the merit of an arm is determined by several, possibly conflicting attributes. The aim is to optimize a 'primary' attribute subject to user-provided constraints on other 'secondary' attributes. We assume that the attributes can be estimated using samples from the arms' distributions, and that the estimators enjoy suitable concentration properties. We propose an algorithm called Con-LCB that guarantees a logarithmic regret, i.e., the average number of plays of all non-optimal arms is at most logarithmic in the horizon. The algorithm also outputs a Boolean flag that correctly identifies, with high probability, whether the given instance is feasible/infeasible with respect to the constraints. We also show that Con-LCB is optimal within a universal constant, i.e., that more sophisticated algorithms cannot do much better universally. Finally, we establish a fundamental trade-off between regret minimization and feasibility identification. Our framework finds natural applications, for instance, in financial portfolio optimization, where risk constrained maximization of expected return is meaningful.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0