Publication

Metrics

AI Quick Summary

This paper constructs a contour map of estimation error for Expected Shortfall (ES), enabling quantitative determination of the necessary sample size for optimizing large institutional portfolios under ES, based on portfolio size, confidence level, and desired error margin.

Paper Preview

Abstract

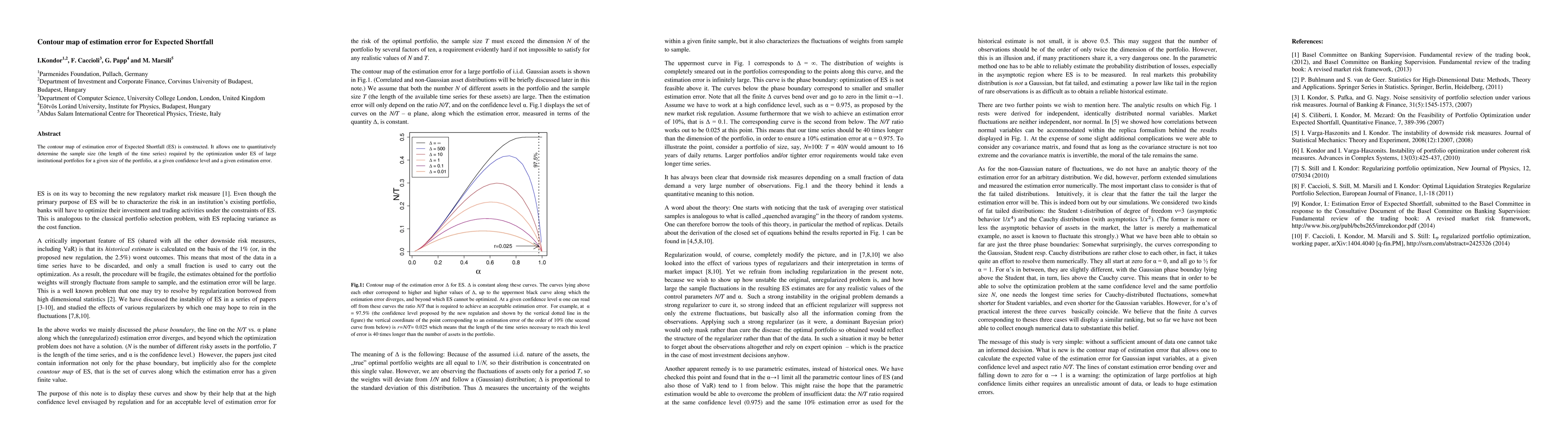

The contour map of estimation error of Expected Shortfall (ES) is constructed. It allows one to quantitatively determine the sample size (the length of the time series) required by the optimization under ES of large institutional portfolios for a given size of the portfolio, at a given confidence level and a given estimation error.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0