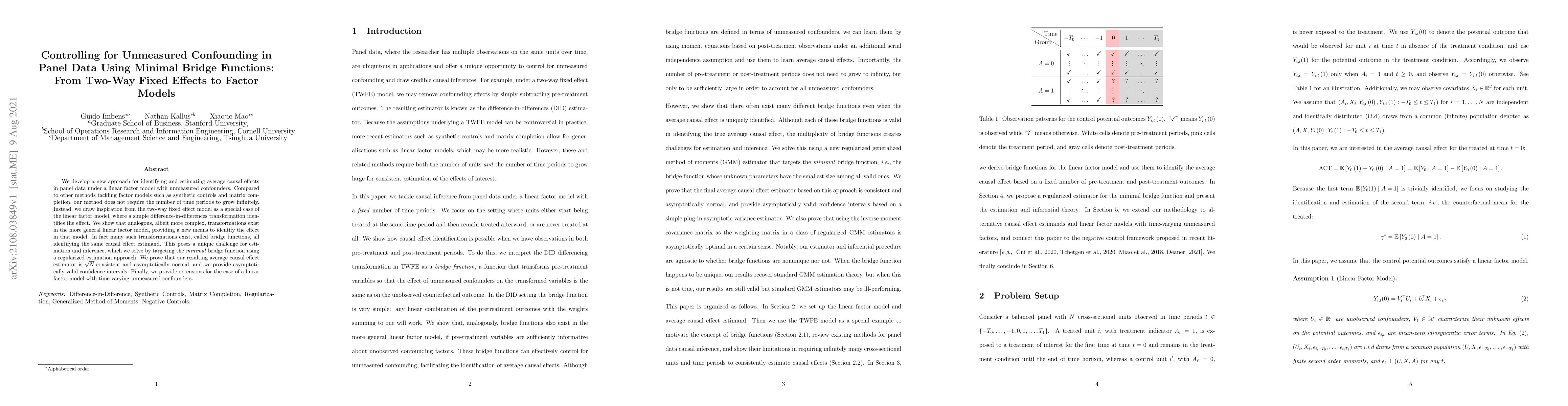

Controlling for Unmeasured Confounding in Panel Data Using Minimal Bridge Functions: From Two-Way Fixed Effects to Factor Models

Publication

Metrics

Paper Preview

Abstract

We develop a new approach for identifying and estimating average causal effects in panel data under a linear factor model with unmeasured confounders. Compared to other methods tackling factor models such as synthetic controls and matrix completion, our method does not require the number of time periods to grow infinitely. Instead, we draw inspiration from the two-way fixed effect model as a special case of the linear factor model, where a simple difference-in-differences transformation identifies the effect. We show that analogous, albeit more complex, transformations exist in the more general linear factor model, providing a new means to identify the effect in that model. In fact many such transformations exist, called bridge functions, all identifying the same causal effect estimand. This poses a unique challenge for estimation and inference, which we solve by targeting the minimal bridge function using a regularized estimation approach. We prove that our resulting average causal effect estimator is root-N consistent and asymptotically normal, and we provide asymptotically valid confidence intervals. Finally, we provide extensions for the case of a linear factor model with time-varying unmeasured confounders.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0