Authors

Summary

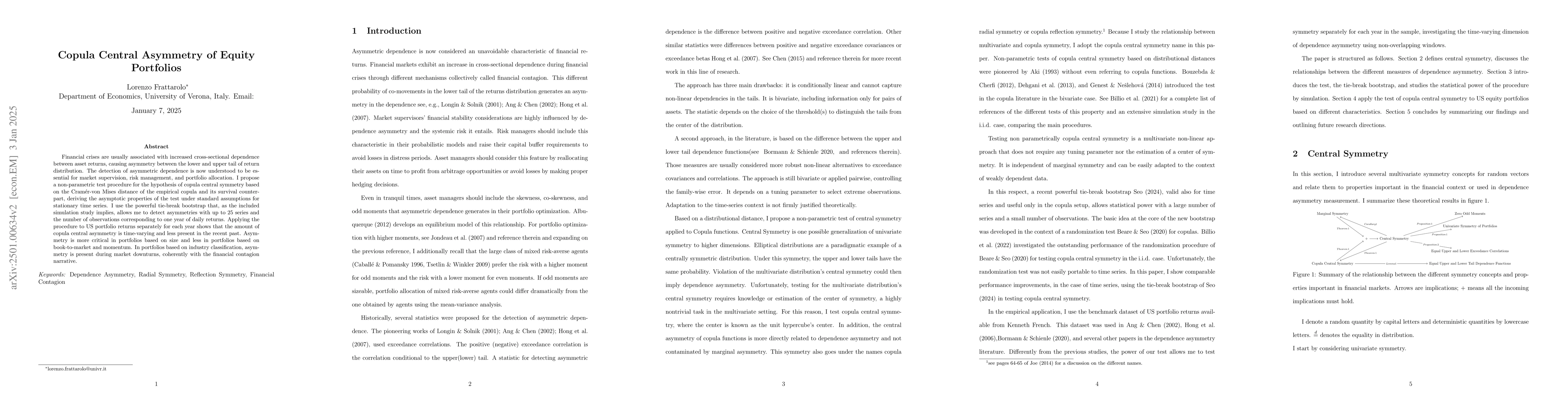

Financial crises are usually associated with increased cross-sectional dependence between asset returns, causing asymmetry between the lower and upper tail of return distribution. The detection of asymmetric dependence is now understood to be essential for market supervision, risk management, and portfolio allocation. I propose a non-parametric test procedure for the hypothesis of copula central symmetry based on the Cram\'er-von Mises distance of the empirical copula and its survival counterpart, deriving the asymptotic properties of the test under standard assumptions for stationary time series. I use the powerful tie-break bootstrap that, as the included simulation study implies, allows me to detect asymmetries with up to 25 series and the number of observations corresponding to one year of daily returns. Applying the procedure to US portfolio returns separately for each year shows that the amount of copula central asymmetry is time-varying and less present in the recent past. Asymmetry is more critical in portfolios based on size and less in portfolios based on book-to-market and momentum. In portfolios based on industry classification, asymmetry is present during market downturns, coherently with the financial contagion narrative.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersOptimization of portfolios with cryptocurrencies: Markowitz and GARCH-Copula model approach

Vahidin Jeleskovic, Zahid I. Younas, Claudio Latini et al.

Large Skew-t Copula Models and Asymmetric Dependence in Intraday Equity Returns

Michael Stanley Smith, Lin Deng, Worapree Maneesoonthorn

No citations found for this paper.

Comments (0)