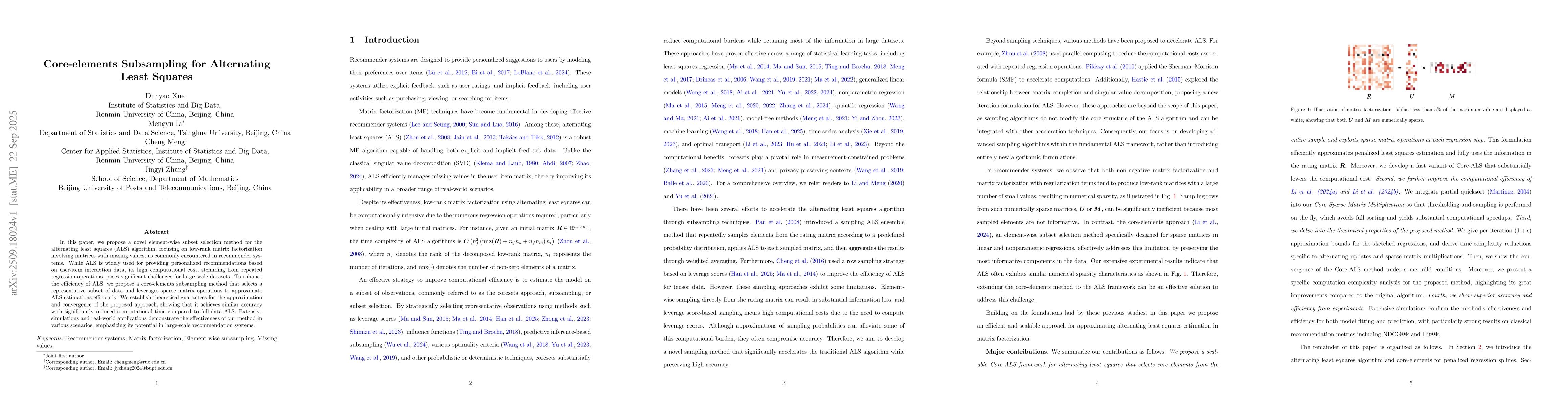

In this paper, we propose a novel element-wise subset selection method for

the alternating least squares (ALS) algorithm, focusing on low-rank matrix

factorization involving matrices with missing values, as commonly encountered

in recommender systems. While ALS is widely used for providing personalized

recommendations based on user-item interaction data, its high computational

cost, stemming from repeated regression operations, poses significant

challenges for large-scale datasets. To enhance the efficiency of ALS, we

propose a core-elements subsampling method that selects a representative subset

of data and leverages sparse matrix operations to approximate ALS estimations

efficiently. We establish theoretical guarantees for the approximation and

convergence of the proposed approach, showing that it achieves similar accuracy

with significantly reduced computational time compared to full-data ALS.

Extensive simulations and real-world applications demonstrate the effectiveness

of our method in various scenarios, emphasizing its potential in large-scale

recommendation systems.

Discussion 0