Publication

Metrics

AI Quick Summary

This paper explores a new currency risk arising from a network of option-based currency volatilities, demonstrating how this network risk influences currency returns. The proposed network strategy, based on causal connections, generates a significant alpha and is uncorrelated with traditional benchmarks.

Paper Preview

Abstract

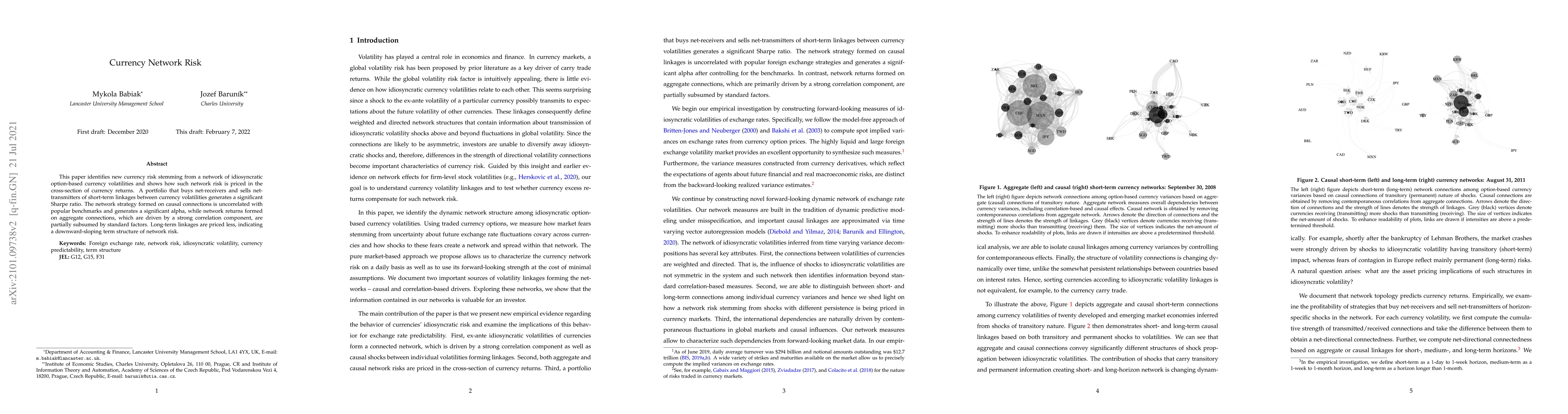

This paper identifies new currency risk stemming from a network of idiosyncratic option-based currency volatilities and shows how such network risk is priced in the cross-section of currency returns. A portfolio that buys net-receivers and sells net-transmitters of short-term linkages between currency volatilities generates a significant Sharpe ratio. The network strategy formed on causal connections is uncorrelated with popular benchmarks and generates a significant alpha, while network returns formed on aggregate connections, which are driven by a strong correlation component, are partially subsumed by standard factors. Long-term linkages are priced less, indicating a downward-sloping term structure of network risk.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0