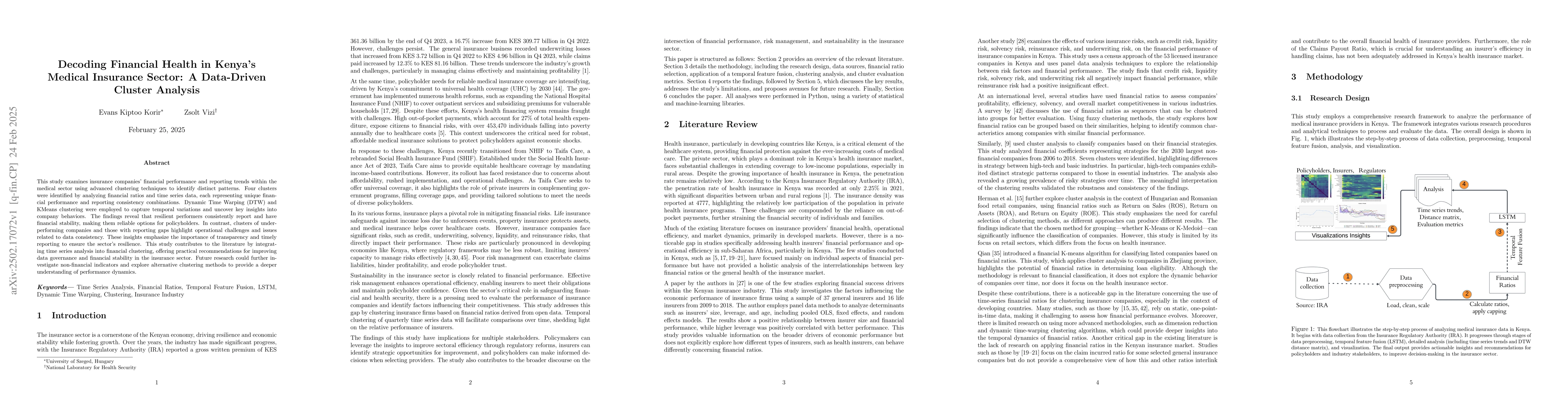

This study examines insurance companies' financial performance and reporting

trends within the medical sector using advanced clustering techniques to

identify distinct patterns. Four clusters were identified by analyzing

financial ratios and time series data, each representing unique financial

performance and reporting consistency combinations. Dynamic Time Warping (DTW)

and KMeans clustering were employed to capture temporal variations and uncover

key insights into company behaviors. The findings reveal that resilient

performers consistently report and have financial stability, making them

reliable options for policyholders. In contrast, clusters of underperforming

companies and those with reporting gaps highlight operational challenges and

issues related to data consistency. These insights emphasize the importance of

transparency and timely reporting to ensure the sector's resilience. This study

contributes to the literature by integrating time series analysis into

financial clustering, offering practical recommendations for improving data

governance and financial stability in the insurance sector. Future research

could further investigate non-financial indicators and explore alternative

clustering methods to provide a deeper understanding of performance dynamics.

Discussion 0