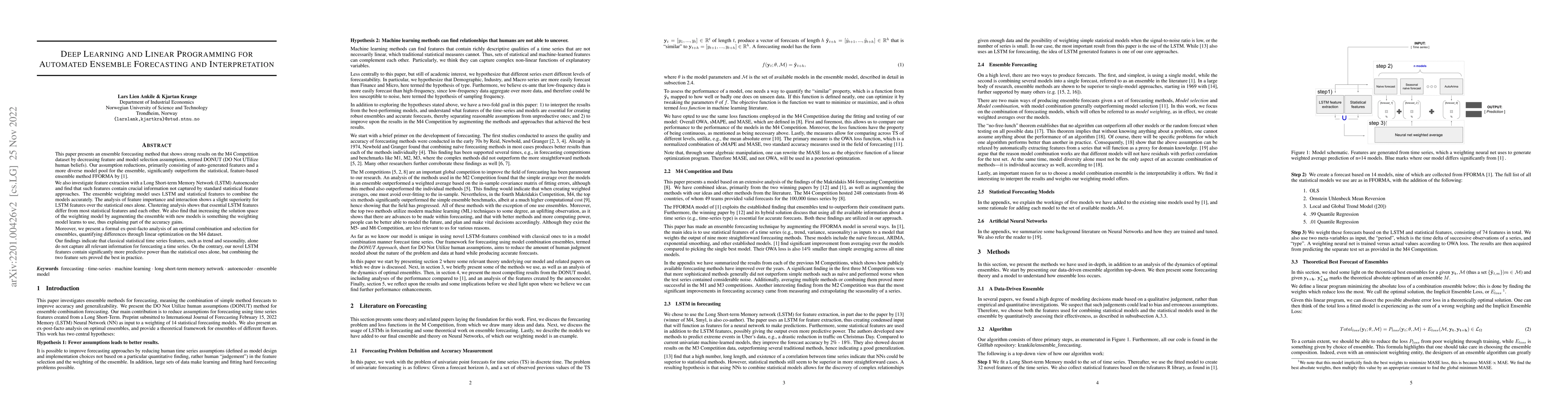

Deep Learning and Linear Programming for Automated Ensemble Forecasting and Interpretation

Publication

Metrics

AI Quick Summary

This paper introduces DONUT, an ensemble forecasting method that outperforms traditional statistical methods by utilizing auto-generated features and a diverse model pool, showing significant gains over FFORMA. The study finds that LSTM features provide crucial predictive information not captured by standard statistical features, and combining both feature types yields the best forecasting results.

Paper Preview

Abstract

This paper presents an ensemble forecasting method that shows strong results on the M4 Competition dataset by decreasing feature and model selection assumptions, termed DONUT (DO Not UTilize human beliefs). Our assumption reductions, primarily consisting of auto-generated features and a more diverse model pool for the ensemble, significantly outperform the statistical, feature-based ensemble method FFORMA by Montero-Manso et al. (2020). We also investigate feature extraction with a Long Short-term Memory Network (LSTM) Autoencoder and find that such features contain crucial information not captured by standard statistical feature approaches. The ensemble weighting model uses LSTM and statistical features to combine the models accurately. The analysis of feature importance and interaction shows a slight superiority for LSTM features over the statistical ones alone. Clustering analysis shows that essential LSTM features differ from most statistical features and each other. We also find that increasing the solution space of the weighting model by augmenting the ensemble with new models is something the weighting model learns to use, thus explaining part of the accuracy gains. Moreover, we present a formal ex-post-facto analysis of an optimal combination and selection for ensembles, quantifying differences through linear optimization on the M4 dataset. Our findings indicate that classical statistical time series features, such as trend and seasonality, alone do not capture all relevant information for forecasting a time series. On the contrary, our novel LSTM features contain significantly more predictive power than the statistical ones alone, but combining the two feature sets proved the best in practice.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0