Depth-Efficient Quantum Topological Data Analysis for Regime-Specific Detection of Financial Stress

Publication

Metrics

Paper Preview

Abstract

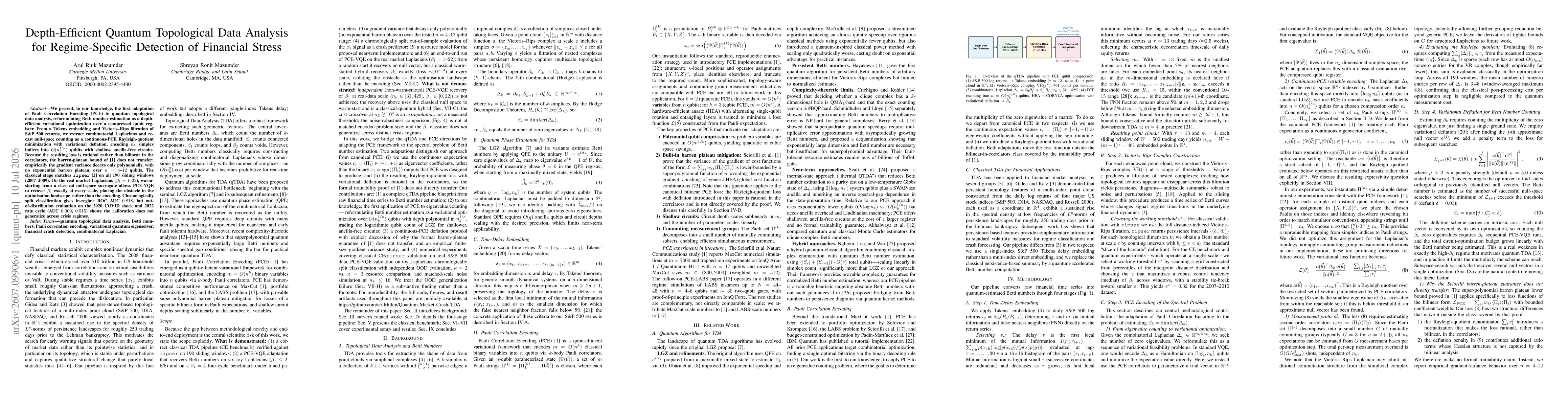

We present, to our knowledge, the first adaptation of Pauli Correlation Encoding (PCE) to quantum topological data analysis, reformulating Betti number estimation as a depth-efficient variational optimization over a compressed qubit register. From a Takens embedding and Vietoris--Rips filtration of S&P~500 returns, we extract combinatorial Laplacians and recast null-space counting as a continuous-PCE Rayleigh-quotient minimization with variational deflation, encoding $n_k$ simplex indices into $O(n_k^{1/κ})$ qubits with shallow, ancilla-free circuits. Because the resulting loss is rational rather than bilinear in the correlators, the barren-plateau bound of~\cite{Sciorilli25} does not transfer; empirically the gradient variance decays only polynomially, with no exponential barren plateau, over $n=4$--$12$ qubits. The classical stage matches ripser~\cite{bauer2021ripser} on all 190 sliding windows (2007-2009). On the real market Laplacians ($β_1=1$--$22$), warm-starting from a classical null-space surrogate allows PCE-VQE to recover $β_1$ exactly at every scale, placing the obstacle in the optimisation landscape rather than the encoding. Chronologically split classification gives in-regime ROC AUC $0.818$, but out-of-distribution evaluation on the 2020 COVID shock and 2022 rate cycle (AUC $0.009$, $0.515$) shows the calibration does not generalize across crisis regimes.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0