Counterfactual reasoning typically involves considering alternatives to

actual events. While often applied to understand past events, a distinct

form-forward counterfactual reasoning-focuses on anticipating plausible future

developments. This type of reasoning is invaluable in dynamic financial

markets, where anticipating market developments can powerfully unveil potential

risks and opportunities for stakeholders, guiding their decision-making.

However, performing this at scale is challenging due to the cognitive demands

involved, underscoring the need for automated solutions. Large Language Models

(LLMs) offer promise, but remain unexplored for this application. To address

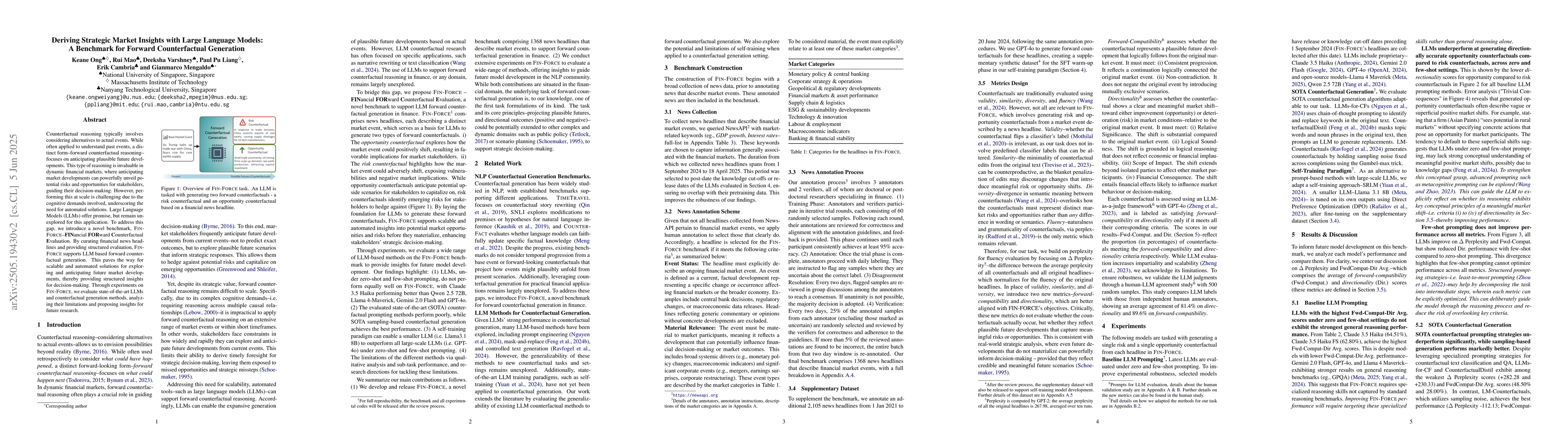

this gap, we introduce a novel benchmark, Fin-Force-FINancial FORward

Counterfactual Evaluation. By curating financial news headlines and providing

structured evaluation, Fin-Force supports LLM based forward counterfactual

generation. This paves the way for scalable and automated solutions for

exploring and anticipating future market developments, thereby providing

structured insights for decision-making. Through experiments on Fin-Force, we

evaluate state-of-the-art LLMs and counterfactual generation methods, analyzing

their limitations and proposing insights for future research.

Discussion 0