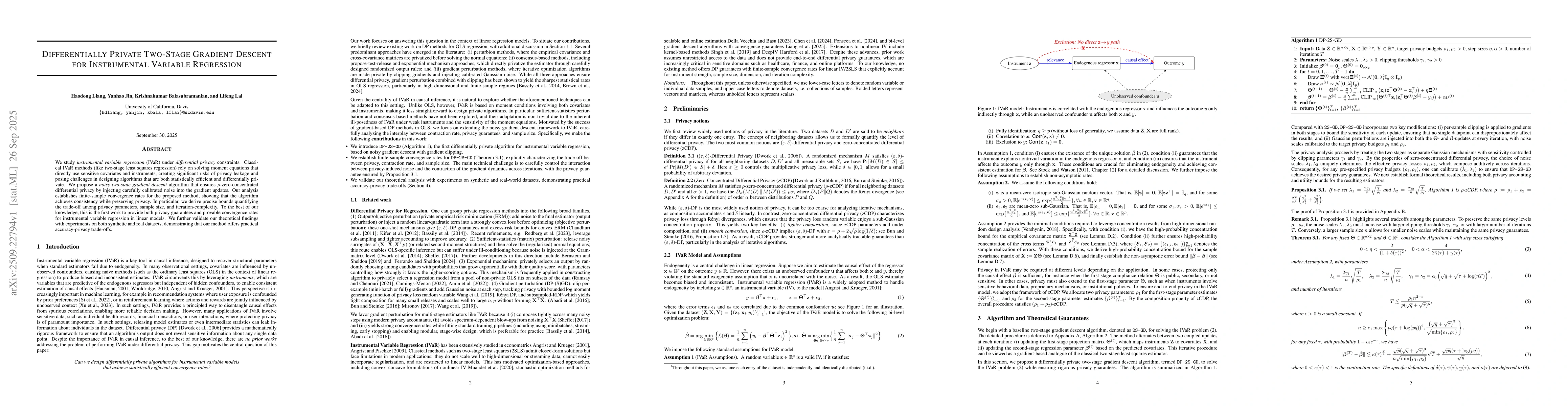

We study instrumental variable regression (IVaR) under differential privacy

constraints. Classical IVaR methods (like two-stage least squares regression)

rely on solving moment equations that directly use sensitive covariates and

instruments, creating significant risks of privacy leakage and posing

challenges in designing algorithms that are both statistically efficient and

differentially private. We propose a noisy two-state gradient descent algorithm

that ensures $\rho$-zero-concentrated differential privacy by injecting

carefully calibrated noise into the gradient updates. Our analysis establishes

finite-sample convergence rates for the proposed method, showing that the

algorithm achieves consistency while preserving privacy. In particular, we

derive precise bounds quantifying the trade-off among privacy parameters,

sample size, and iteration-complexity. To the best of our knowledge, this is

the first work to provide both privacy guarantees and provable convergence

rates for instrumental variable regression in linear models. We further

validate our theoretical findings with experiments on both synthetic and real

datasets, demonstrating that our method offers practical accuracy-privacy

trade-offs.

Discussion 0