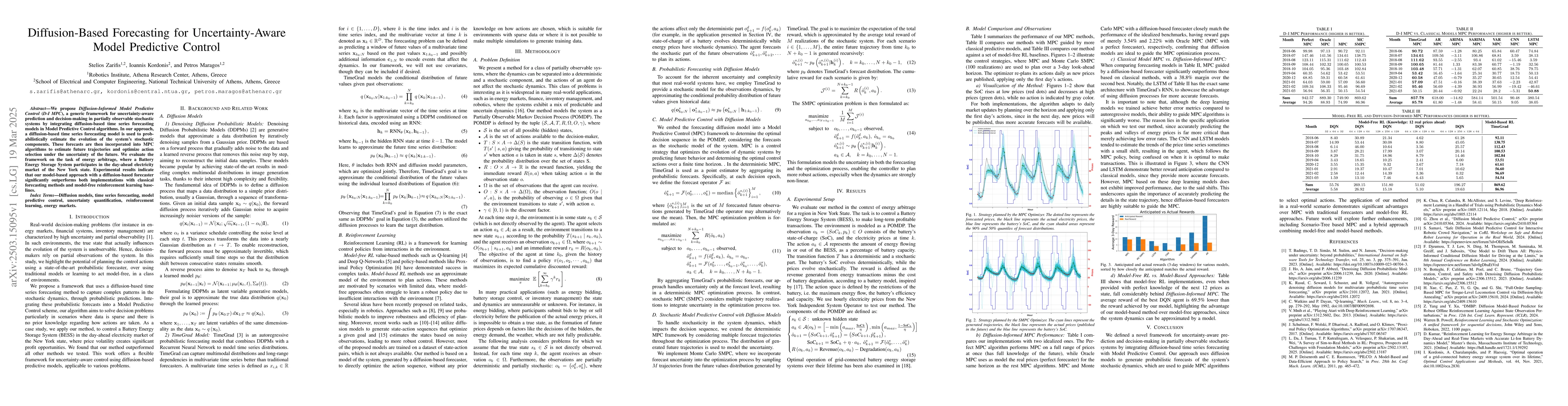

We propose Diffusion-Informed Model Predictive Control (D-I MPC), a generic

framework for uncertainty-aware prediction and decision-making in partially

observable stochastic systems by integrating diffusion-based time series

forecasting models in Model Predictive Control algorithms. In our approach, a

diffusion-based time series forecasting model is used to probabilistically

estimate the evolution of the system's stochastic components. These forecasts

are then incorporated into MPC algorithms to estimate future trajectories and

optimize action selection under the uncertainty of the future. We evaluate the

framework on the task of energy arbitrage, where a Battery Energy Storage

System participates in the day-ahead electricity market of the New York state.

Experimental results indicate that our model-based approach with a

diffusion-based forecaster significantly outperforms both implementations with

classical forecasting methods and model-free reinforcement learning baselines.

Discussion 0