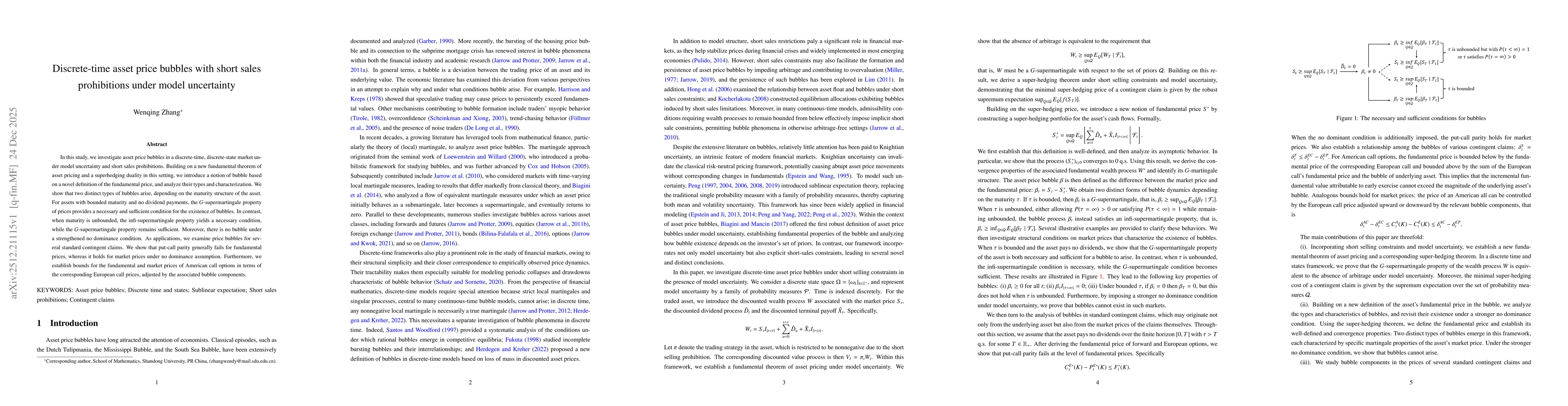

In this study, we investigate asset price bubbles in a discrete-time, discrete-state market under model uncertainty and short sales prohibitions. Building on a new fundamental theorem of asset pricing and a superhedging duality in this setting, we introduce a notion of bubble based on a novel definition of the fundamental price, and analyze their types and characterization. We show that two distinct types of bubbles arise, depending on the maturity structure of the asset. For assets with bounded maturity and no dividend payments, the $G$-supermartingale property of prices provides a necessary and sufficient condition for the existence of bubbles. In contrast, when maturity is unbounded, the infi-supermartingale property yields a necessary condition, while the $G$-supermartingale property remains sufficient. Moreover, there is no bubble under a strengthened no dominance condition. As applications, we examine price bubbles for several standard contingent claims. We show that put-call parity generally fails for fundamental prices, whereas it holds for market prices under no dominance assumption. Furthermore, we establish bounds for the fundamental and market prices of American call options in terms of the corresponding European call prices, adjusted by the associated bubble components.

Discussion 0