Publication

Metrics

AI Quick Summary

This paper proposes a distribution-free pricing policy for contextual dynamic pricing where the seller learns customer valuations based on contextual information and purchase feedback without knowing the random noise distribution. The method employs a novel perturbed linear bandit framework to balance exploration and exploitation, achieving sub-linear regret bounds and demonstrating superior performance in simulations and real-life data.

Paper Preview

Abstract

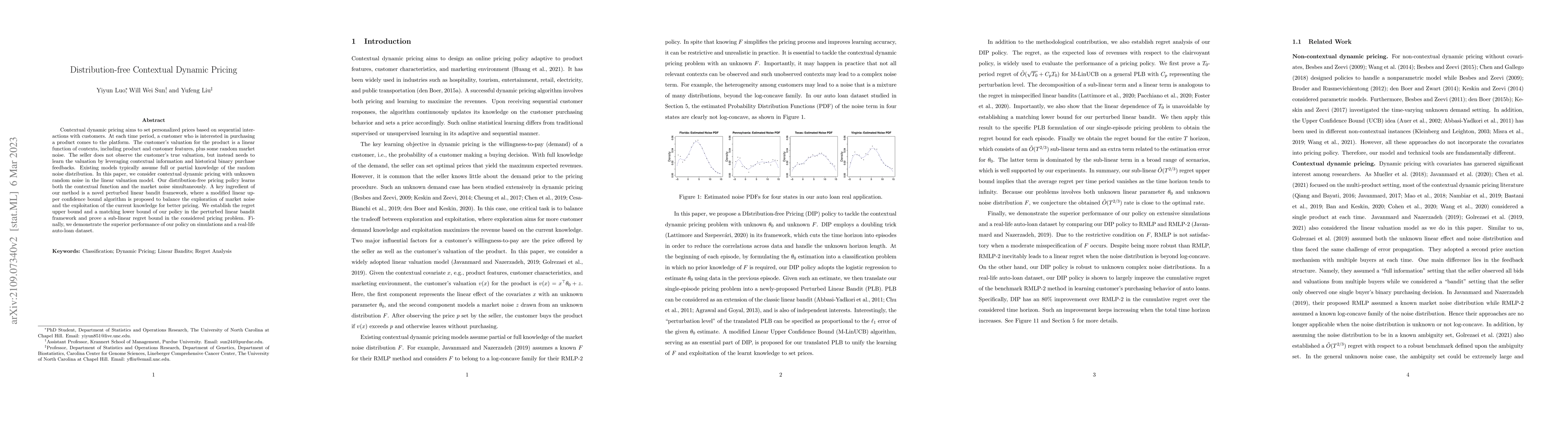

Contextual dynamic pricing aims to set personalized prices based on sequential interactions with customers. At each time period, a customer who is interested in purchasing a product comes to the platform. The customer's valuation for the product is a linear function of contexts, including product and customer features, plus some random market noise. The seller does not observe the customer's true valuation, but instead needs to learn the valuation by leveraging contextual information and historical binary purchase feedbacks. Existing models typically assume full or partial knowledge of the random noise distribution. In this paper, we consider contextual dynamic pricing with unknown random noise in the valuation model. Our distribution-free pricing policy learns both the contextual function and the market noise simultaneously. A key ingredient of our method is a novel perturbed linear bandit framework, where a modified linear upper confidence bound algorithm is proposed to balance the exploration of market noise and the exploitation of the current knowledge for better pricing. We establish the regret upper bound and a matching lower bound of our policy in the perturbed linear bandit framework and prove a sub-linear regret bound in the considered pricing problem. Finally, we demonstrate the superior performance of our policy on simulations and a real-life auto-loan dataset.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0