Dynamic Bayesian Networks with Conditional Dynamics in Edge Addition and Deletion

Publication

Metrics

AI Quick Summary

This paper introduces a dynamic Bayesian network model that allows for intuitive gradual changes in edge additions and deletions using conditional dynamics. Unlike previous methods, it achieves more frequent and clear network evolution, and employs MCMC sampling for parameter estimation, demonstrated through a portfolio selection application.

Paper Preview

Abstract

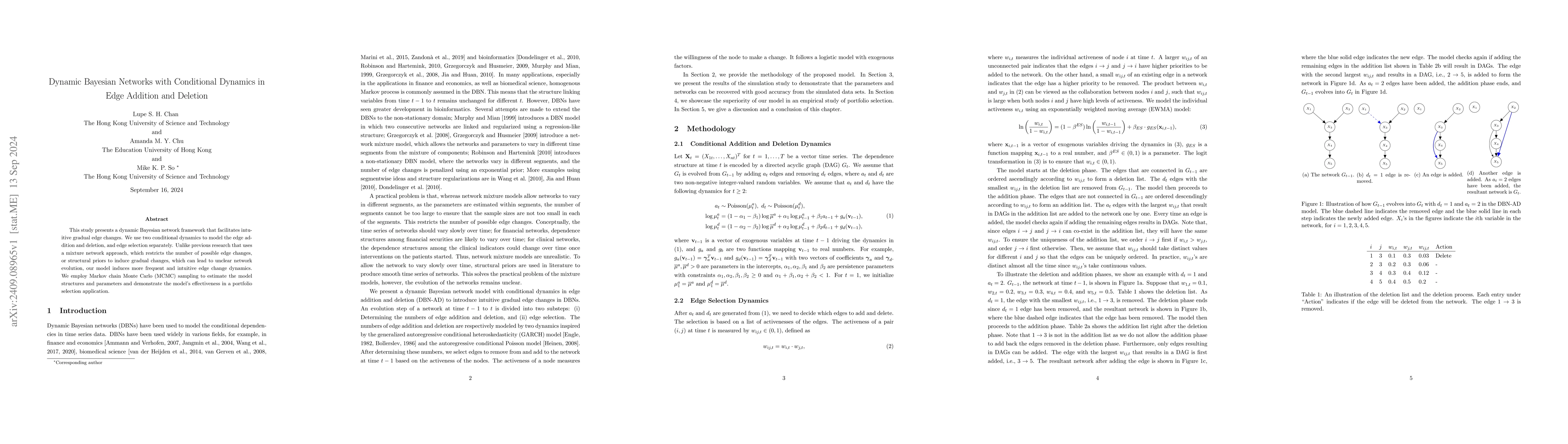

This study presents a dynamic Bayesian network framework that facilitates intuitive gradual edge changes. We use two conditional dynamics to model the edge addition and deletion, and edge selection separately. Unlike previous research that uses a mixture network approach, which restricts the number of possible edge changes, or structural priors to induce gradual changes, which can lead to unclear network evolution, our model induces more frequent and intuitive edge change dynamics. We employ Markov chain Monte Carlo (MCMC) sampling to estimate the model structures and parameters and demonstrate the model's effectiveness in a portfolio selection application.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0