Background

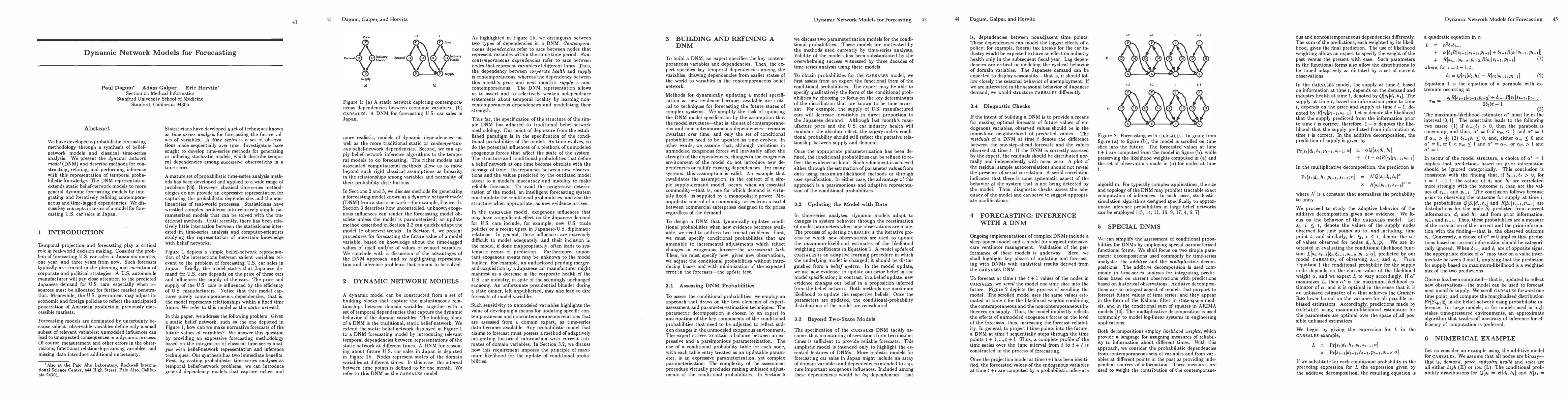

Forecasting typically relies on time-series analysis, which models sequential observations but often assumes linear, Gaussian structure or other simplifying parametric forms. Static belief networks, meanwhile, encode probabilistic dependencies among variables at a single time point but lack a principled, scalable way to model dynamics. The authors argue that real-world forecasting benefits from a synthesis of these traditions: a dynamic, probabilistic model that can capture how variables influence each other over time, including nonlinear and non-Gaussian relationships. The CARSALES example grounds the discussion, showing a static network of contemporaneous economic relations and how it can be extended into a dynamic forecasting model.

Problem / Research Question

The central question is how to forecast future values of variables when the underlying domain exhibits temporal evolution and is subject to unmodeled, exogenous influences. Specifically, how can one extend a static belief-network representation to a dynamic setting that supports time-lagged dependencies, adaptive updating, and robust forecasting, without being overwhelmed by model mis-specification or computational intractability?

Innovation / Contribution

The core contribution is the Dynamic Network Model (DNM), which generalizes static belief networks to dynamic forecasting by incorporating temporal dependencies. DNMs distinguish two dependency types: contemporaneous edges (within the same time slice) and non-contemporaneous edges (connecting across time slices). This enables richer representations of how domain variables interact over time and how past states influence future outcomes. A key technical novelty is the adaptive updating mechanism: as new observations arrive, the model updates conditional probabilities (and potentially structure) to reflect observed trends, guided by maximum-likelihood principles to avoid drifting due to unmodeled exogenous forces.

Methodology / Approach

DNMs are built by starting from a static network that encodes instantaneous dependencies, then generating a time-indexed tower of such networks for successive time points. Temporal dependencies link variables across adjacent (or multiple) time steps, with a chosen time interval (the CARSALES example uses one month). Inference in the dynamic model uses belief-network techniques to compute forecasts for future states given observed data. Exogenous influences—like policy changes or market shocks—are explicitly acknowledged as potentially unknown and are managed by updating (and potentially adjusting) the conditional dependencies as evidence accumulates. The approach emphasizes adaptivity: structure and probabilities are not fixed forever but can be revised to maintain forecast accuracy.

Experiments / Evaluation

From the excerpts, the authors illustrate the approach via a concrete model for forecasting U.S. car sales in Japan (CARSALES). They describe the modeling choices, the distinction between contemporaneous and non-contemporaneous relationships, and the updating mechanism, but the provided pages do not present quantitative empirical results or benchmark comparisons. The evaluation, as described, centers on the conceptual demonstration of a DNM and its ability to respond to changing information rather than on reported experimental metrics.

Key Results

The material presents a coherent blueprint and qualitative justification for dynamic, probabilistic forecasting. It emphasizes two immediate benefits: (i) DNMs provide richer representations of dynamic dependencies that go beyond linear, normal-distribution assumptions, and (ii) belief-network inference techniques can be applied to temporal models to produce forecasts and facilitate decision support. While the CARSALES case demonstrates the modeling approach, concrete performance results, quantitative metrics, or comparative studies are not disclosed in the excerpt.

Practical Applications

DNMs are intended for forecasting and control in domains where detailed knowledge about dynamic forces exists but complete specification is impractical. Potential applications include economics and business planning (as illustrated by car sales forecasting), operations research, and healthcare informatics, where temporal dynamics and uncertain exogenous events play crucial roles. The framework supports continual updating and adaptation, making it suitable for environments characterized by evolving policy, market conditions, or patient states, where rapid, probabilistic reasoning is valuable for planning and intervention.

Limitations & Considerations

Key considerations include the computational complexity of inference in time-extended networks and the challenge of selecting appropriate time lags and structures. The authors acknowledge that exogenous influences can destabilize naïve models and require adaptive updating; however, the criteria and procedures for when to alter structure versus parameters remain open. Practical deployment requires robust learning algorithms, methods for structure learning in DNMs, and rigorous empirical validation across domains and data regimes. The discussion also hints at the need for improved methods to induce DNMs from static networks using time-series data, which remains an area for future work.

Discussion 0