Publication

Metrics

AI Quick Summary

The paper develops an early asset-pricing framework for compute power, showing that traditional futures pricing fails because compute is non-storable, and synthetic futures from rental contracts likely bound true futures. Using these synthetic futures, the authors construct a compute futures return panel by GPU generation and maturity, finding preliminary evidence of a positive compute risk premium, implying hedging pressure on compute providers as the market for compute futures evolves.

Paper Preview

Abstract

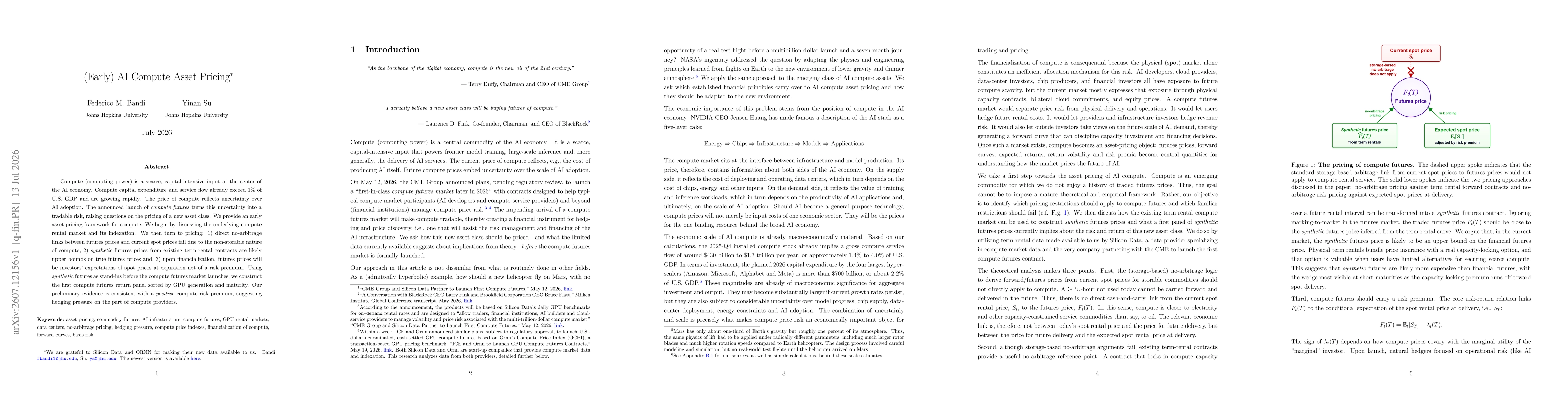

Compute (computing power) is a scarce, capital-intensive input at the center of the AI economy. Compute capital expenditure and service flow already exceed 1% of U.S. GDP and are growing rapidly. The price of compute reflects uncertainty over AI adoption. The announced launch of compute futures turns this uncertainty into a tradable risk, raising questions on the pricing of a new asset class. We provide an early asset-pricing framework for compute. We begin by discussing the underlying compute rental market and its indexation. We then turn to pricing: 1) direct no-arbitrage links between futures prices and current spot prices fail due to the non-storable nature of compute, 2) synthetic futures prices from existing term rental contracts are likely upper bounds on true futures prices and, 3) upon financialization, futures prices will be investors' expectations of spot prices at expiration net of a risk premium. Using synthetic futures as stand-ins before the compute futures market launches, we construct the first compute futures return panel sorted by GPU generation and maturity. Our preliminary evidence is consistent with a positive compute risk premium, suggesting hedging pressure on the part of compute providers.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0