Authors

Summary

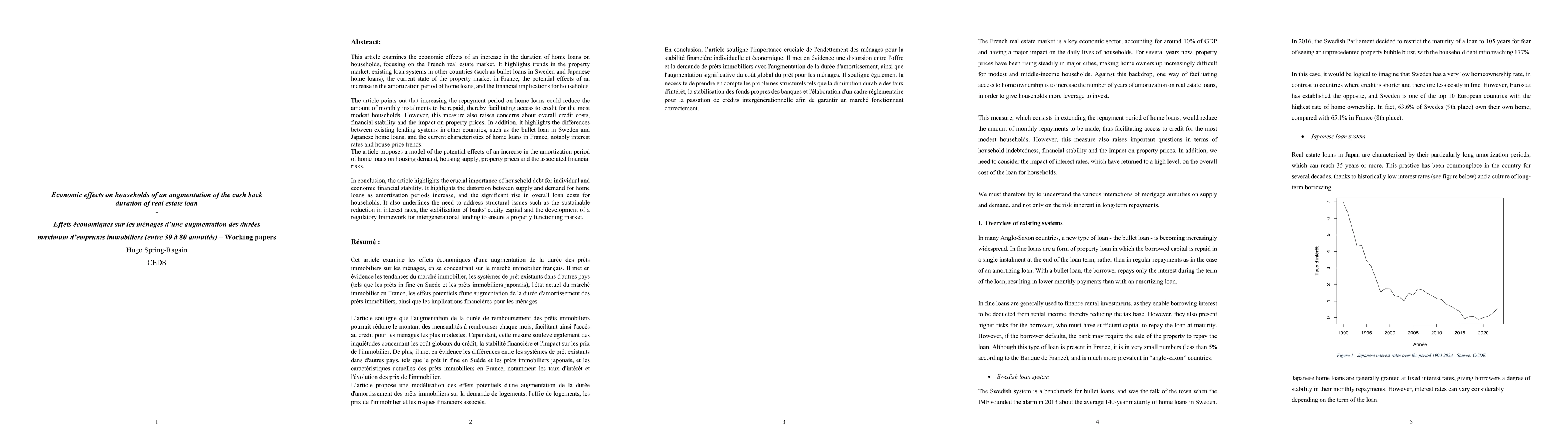

This article examines the economic effects of an increase in the duration of home loans on households, focusing on the French real estate market. It highlights trends in the property market, existing loan systems in other countries (such as bullet loans in Sweden and Japanese home loans), the current state of the property market in France, the potential effects of an increase in the amortization period of home loans, and the financial implications for households.The article points out that increasing the repayment period on home loans could reduce the amount of monthly instalments to be repaid, thereby facilitating access to credit for the most modest households. However, this measure also raises concerns about overall credit costs, financial stability and the impact on property prices. In addition, it highlights the differences between existing lending systems in other countries, such as the bullet loan in Sweden and Japanese home loans, and the current characteristics of home loans in France, notably interest rates and house price trends. The article proposes a model of the potential effects of an increase in the amortization period of home loans on housing demand, housing supply, property prices and the associated financial risks.In conclusion, the article highlights the crucial importance of household debt for individual and economic financial stability. It highlights the distortion between supply and demand for home loans as amortization periods increase, and the significant rise in overall loan costs for households. It also underlines the need to address structural issues such as the sustainable reduction in interest rates, the stabilization of banks' equity capital and the development of a regulatory framework for intergenerational lending to ensure a properly functioning market.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersThe loss optimisation of loan recovery decision times using forecast cash flows

Arno Botha, Conrad Beyers, Pieter de Villiers

Analyzing the Impact of Tax Credits on Households in Simulated Economic Systems with Learning Agents

Svitlana Vyetrenko, Jialin Dong, Kshama Dwarakanath

No citations found for this paper.

Comments (0)