Economic Integration and Agglomeration of Multinational Production with Transfer Pricing

Publication

Metrics

AI Quick Summary

This paper explores how low corporate taxes affect multinational production and economic integration, finding that falling trade costs can initially increase production in high-tax countries before reversing. It also highlights that transfer pricing complicates tax competition, suggesting international coordination on transfer-pricing regulation could be beneficial.

Paper Preview

Abstract

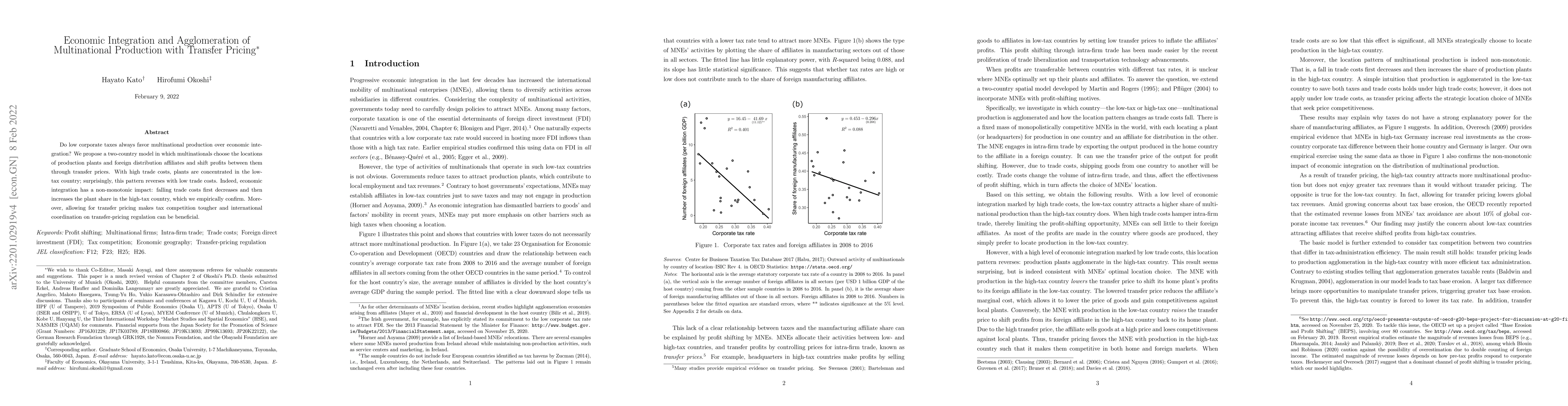

Do low corporate taxes always favor multinational production over economic integration? We propose a two-country model in which multinationals choose the locations of production plants and foreign distribution affiliates and shift profits between them through transfer prices. With high trade costs, plants are concentrated in the low-tax country; surprisingly, this pattern reverses with low trade costs. Indeed, economic integration has a non-monotonic impact: falling trade costs first decrease and then increase the plant share in the high-tax country, which we empirically confirm. Moreover, allowing for transfer pricing makes tax competition tougher and international coordination on transfer-pricing regulation can be beneficial.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0