Efficient nonparametric estimation and inference for the volatility function

Publication

Metrics

AI Quick Summary

This paper proposes a nonparametric method for estimating and inferring the volatility function in financial data, offering tools for model evaluation and a new representation of the GARCH(1,1) model. Simulation results show that the proposed method outperforms the MLE estimator of GARCH(1,1) even under correct model specification.

Paper Preview

Abstract

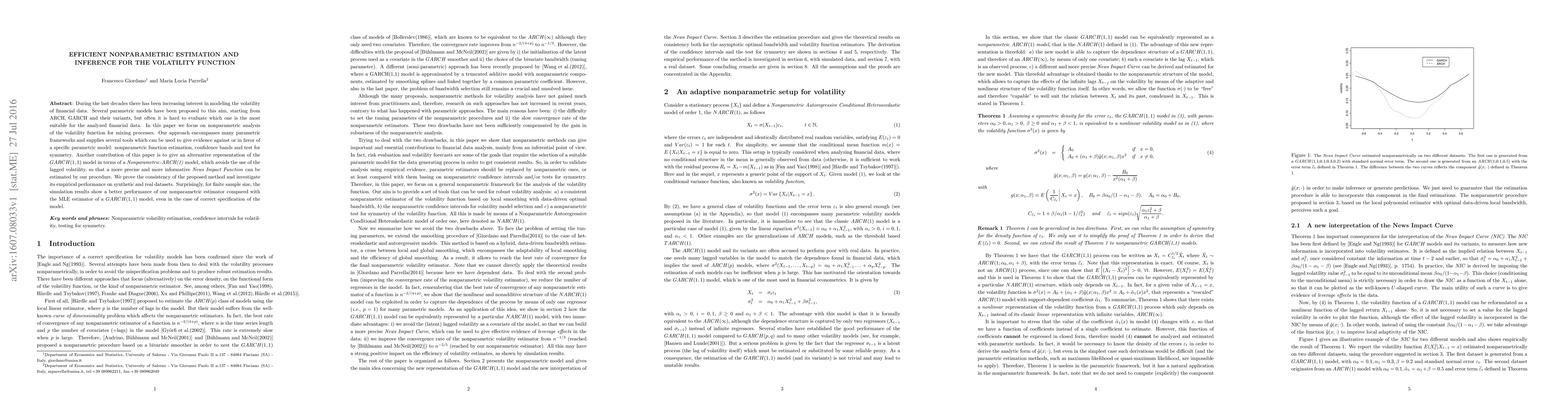

During the last decades there has been increasing interest in modeling the volatility of financial data. Several parametric models have been proposed to this aim, starting from ARCH, GARCH and their variants, but often it is hard to evaluate which one is the most suitable for the analyzed financial data. In this paper we focus on nonparametric analysis of the volatility function for mixing processes. Our approach encompasses many parametric frameworks and supplies several tools which can be used to give evidence against or in favor of a specific parametric model: nonparametric function estimation, confidence bands and test for symmetry. Another contribution of this paper is to give an alternative representation of the GARCH(1,1) model in terms of a Nonparametric-ARCH(1) model, which avoids the use of the lagged volatility, so that a more precise and more informative News Impact Function can be estimated by our procedure. We prove the consistency of the proposed method and investigate its empirical performance on synthetic and real datasets. Surprisingly, for finite sample size, the simulation results show a better performance of our nonparametric estimator compared with the MLE estimator of a GARCH(1,1) model, even in the case of correct specification of the model.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0