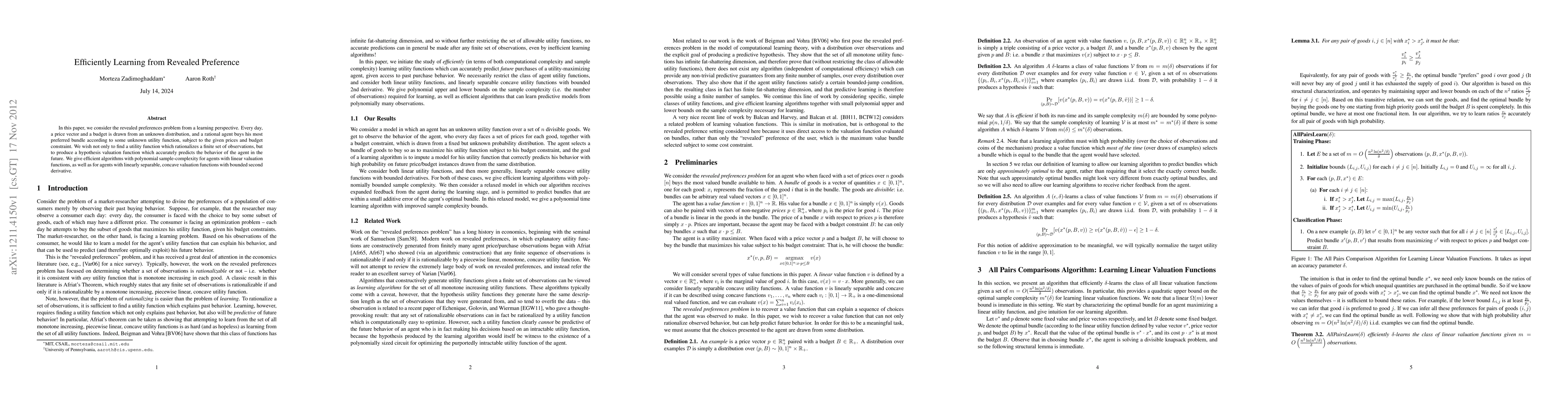

Efficiently Learning from Revealed Preference

Publication

Metrics

AI Quick Summary

Researchers developed efficient algorithms to learn a utility function from revealed preference data, allowing accurate predictions of future behavior in rational agents with linear or concave valuation functions.

Paper Preview

Abstract

In this paper, we consider the revealed preferences problem from a learning perspective. Every day, a price vector and a budget is drawn from an unknown distribution, and a rational agent buys his most preferred bundle according to some unknown utility function, subject to the given prices and budget constraint. We wish not only to find a utility function which rationalizes a finite set of observations, but to produce a hypothesis valuation function which accurately predicts the behavior of the agent in the future. We give efficient algorithms with polynomial sample-complexity for agents with linear valuation functions, as well as for agents with linearly separable, concave valuation functions with bounded second derivative.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0