Enhancing Few-Shot Stock Trend Prediction with Large Language Models

Publication

Metrics

AI Quick Summary

This paper proposes using Large Language Models (LLMs) in a few-shot setting to predict stock trends without extensive annotated data. It introduces a 'denoising-then-voting' two-step method to classify individual news as relevant or irrelevant and aggregates predictions, achieving accuracy rates of 66.59% for S&P 500, 62.17% for CSI-100, and 61.17% for HK stocks, outperforming standard few-shot methods by 7%, 4%, and 4% respectively.

Paper Preview

Abstract

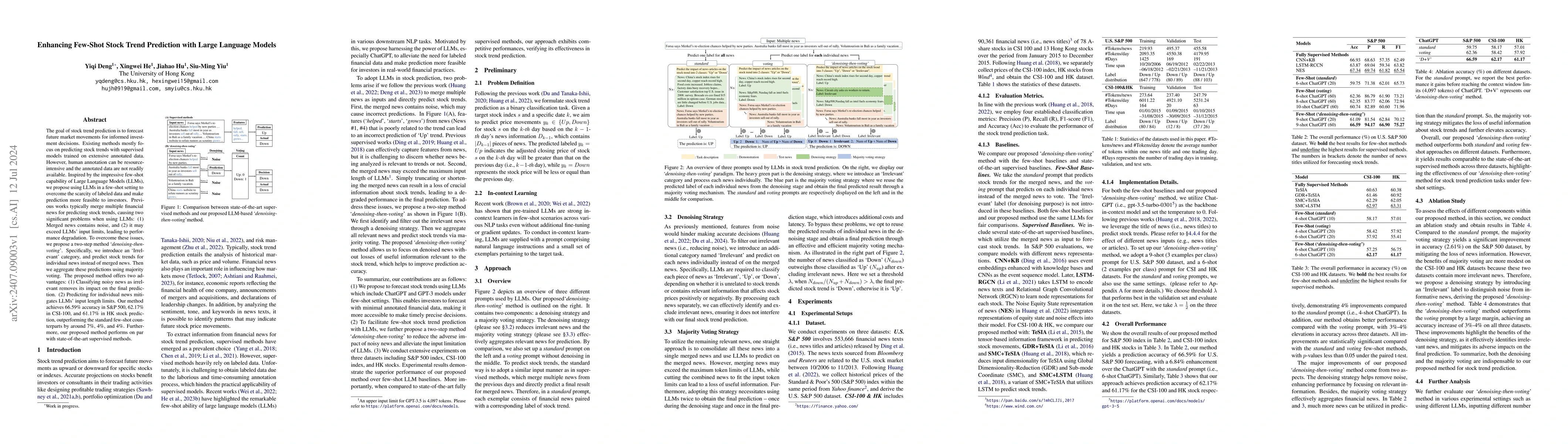

The goal of stock trend prediction is to forecast future market movements for informed investment decisions. Existing methods mostly focus on predicting stock trends with supervised models trained on extensive annotated data. However, human annotation can be resource-intensive and the annotated data are not readily available. Inspired by the impressive few-shot capability of Large Language Models (LLMs), we propose using LLMs in a few-shot setting to overcome the scarcity of labeled data and make prediction more feasible to investors. Previous works typically merge multiple financial news for predicting stock trends, causing two significant problems when using LLMs: (1) Merged news contains noise, and (2) it may exceed LLMs' input limits, leading to performance degradation. To overcome these issues, we propose a two-step method 'denoising-then-voting'. Specifically, we introduce an `Irrelevant' category, and predict stock trends for individual news instead of merged news. Then we aggregate these predictions using majority voting. The proposed method offers two advantages: (1) Classifying noisy news as irrelevant removes its impact on the final prediction. (2) Predicting for individual news mitigates LLMs' input length limits. Our method achieves 66.59% accuracy in S&P 500, 62.17% in CSI-100, and 61.17% in HK stock prediction, outperforming the standard few-shot counterparts by around 7%, 4%, and 4%. Furthermore, our proposed method performs on par with state-of-the-art supervised methods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0