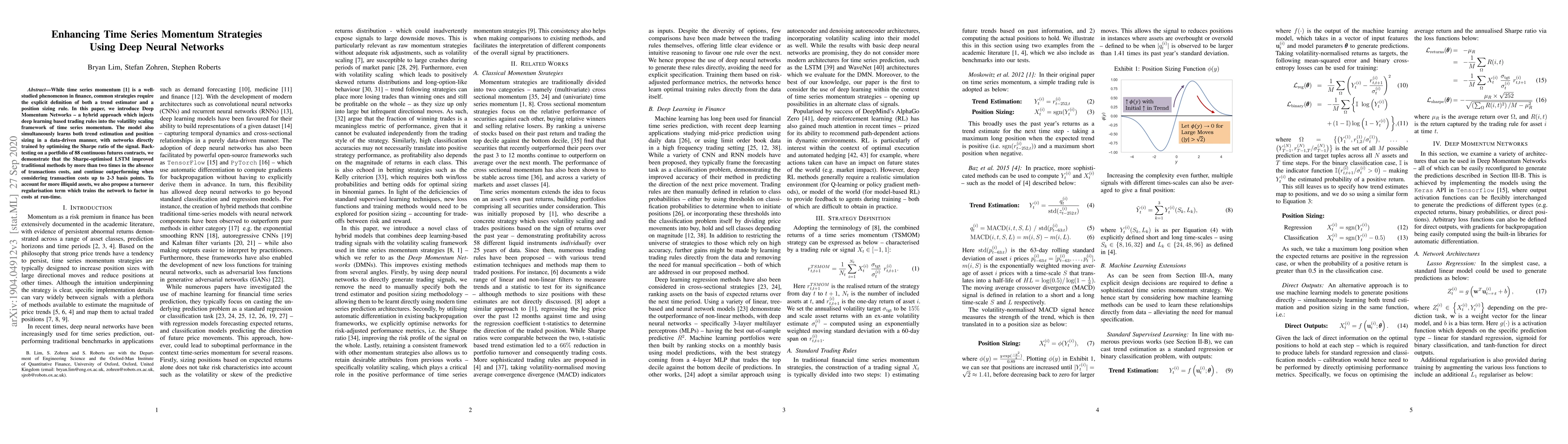

While time series momentum is a well-studied phenomenon in finance, common

strategies require the explicit definition of both a trend estimator and a

position sizing rule. In this paper, we introduce Deep Momentum Networks -- a

hybrid approach which injects deep learning based trading rules into the

volatility scaling framework of time series momentum. The model also

simultaneously learns both trend estimation and position sizing in a

data-driven manner, with networks directly trained by optimising the Sharpe

ratio of the signal. Backtesting on a portfolio of 88 continuous futures

contracts, we demonstrate that the Sharpe-optimised LSTM improved traditional

methods by more than two times in the absence of transactions costs, and

continue outperforming when considering transaction costs up to 2-3 basis

points. To account for more illiquid assets, we also propose a turnover

regularisation term which trains the network to factor in costs at run-time.

Discussion 0