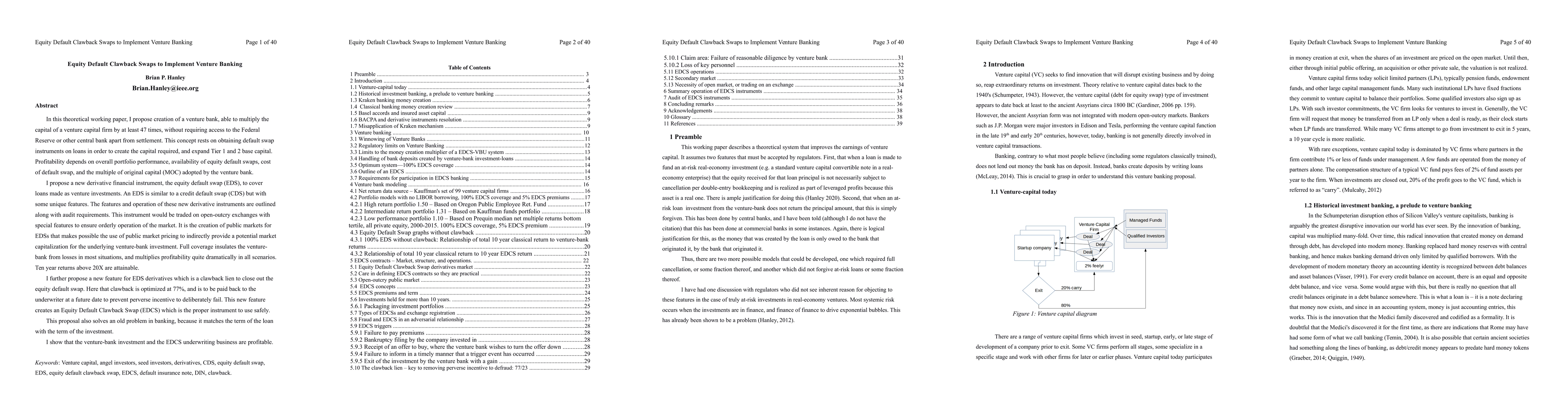

In this theoretical paper, I propose creation of a venture bank, able to

multiply the capital of a venture capital firm by at least 47 times, without

requiring access to the Federal Reserve or other central bank apart from

settlement. This concept rests on obtaining default swap instruments on loans

in order to create the capital required, and expand Tier 1 and 2 base capital.

Profitability depends on overall portfolio performance, availability of equity

default swaps, cost of default swap, and the multiple of original capital (MOC)

adopted by the venture bank. A new derivative financial instrument, the equity

default swap (EDS), to cover loans made as venture investments. An EDS is

similar to a credit default swap (CDS) but with some unique features. The

features and operation of these new derivative instruments are outlined along

with audit requirements. This instrument would be traded on open-outcry

exchanges with special features to ensure orderly operation of the market. It

is the creation of public markets for EDSs that makes possible the use of

public market pricing to indirectly provide a potential market capitalization

for the underlying venture-bank investment. Full coverage insulates the

venture-bank from losses in most situations, and multiplies profitability quite

dramatically in all scenarios. Ten year returns above 20X are attainable.

Further, a new feature for EDS derivatives, a clawback lien, closes out the

equity default swap. Here it is optimized at 77%, and is to be paid back to the

underwriter at a future date to prevent perverse incentive to deliberately

fail. This new feature creates an Equity Default Clawback Swap (EDCS) which can

be used safely. This proposal also solves an old problem in banking, because it

matches the term of the loan with the term of the investment. I show that the

venture-bank investment and the EDCS underwriting business are profitable.

Discussion 0