Ergodicity-breaking reveals time optimal decision making in humans

Publication

Metrics

AI Quick Summary

This paper explores how human decision-making adapts to different gamble dynamics, finding that risk aversion increases under multiplicative dynamics to optimize wealth growth over time, challenging traditional ergodic theories and suggesting a need for new decision-making frameworks.

Paper Preview

Abstract

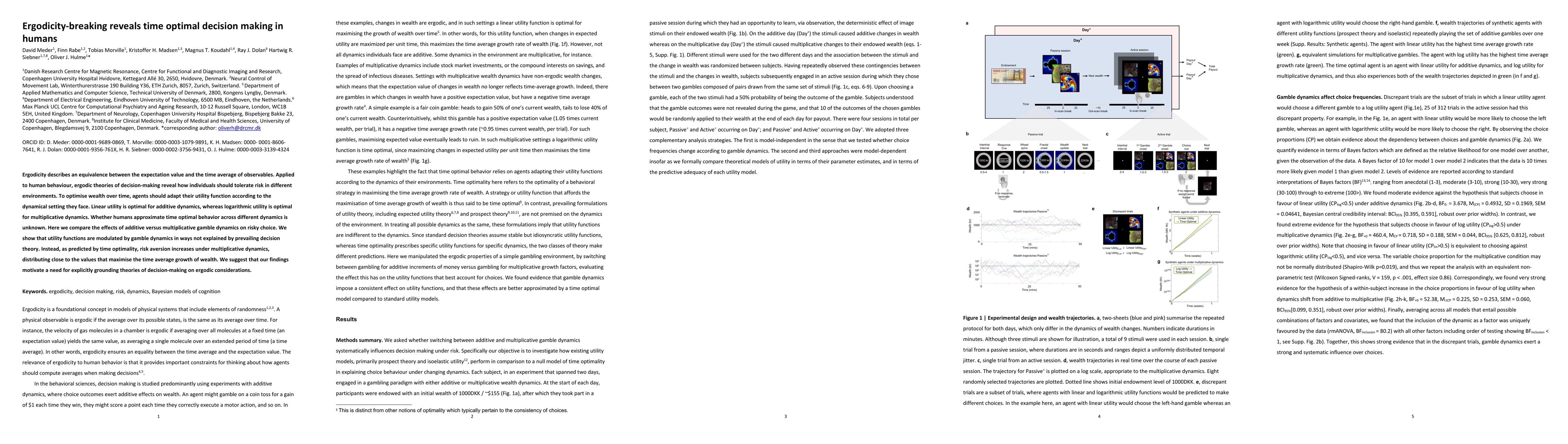

Ergodicity describes an equivalence between the expectation value and the time average of observables. Applied to human behaviour, ergodic theories of decision-making reveal how individuals should tolerate risk in different environments. To optimise wealth over time, agents should adapt their utility function according to the dynamical setting they face. Linear utility is optimal for additive dynamics, whereas logarithmic utility is optimal for multiplicative dynamics. Whether humans approximate time optimal behavior across different dynamics is unknown. Here we compare the effects of additive versus multiplicative gamble dynamics on risky choice. We show that utility functions are modulated by gamble dynamics in ways not explained by prevailing decision theory. Instead, as predicted by time optimality, risk aversion increases under multiplicative dynamics, distributing close to the values that maximise the time average growth of wealth. We suggest that our findings motivate a need for explicitly grounding theories of decision-making on ergodic considerations.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0