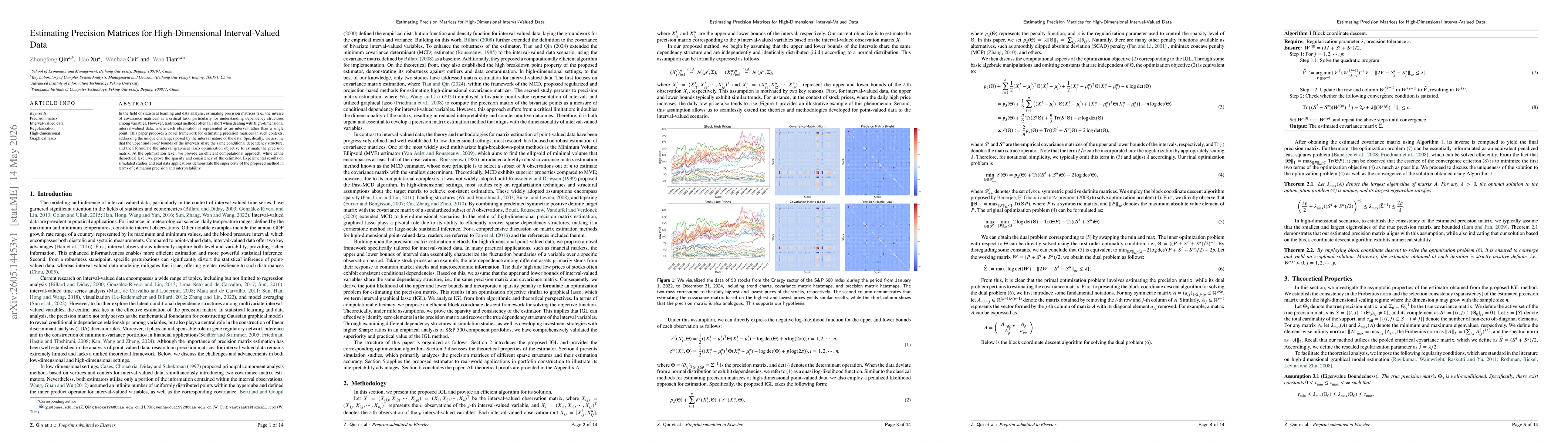

01

MethodologyHow they did it

We formulate Interval Graphical Lasso (IGL) by assuming the upper and lower bounds of interval-valued variables share the same conditional dependency structure and derive a joint likelihood for the interval endpoints. The objective combines a log-determinant term with an l1-penalty to promote sparsity in the precision matrix, and we develop a block coordinate descent algorithm to efficiently solve the optimization under mild regularity conditions.

Discussion 0