Estimation of scale functions to model heteroscedasticity by support vector machines

Publication

Metrics

Paper Preview

Abstract

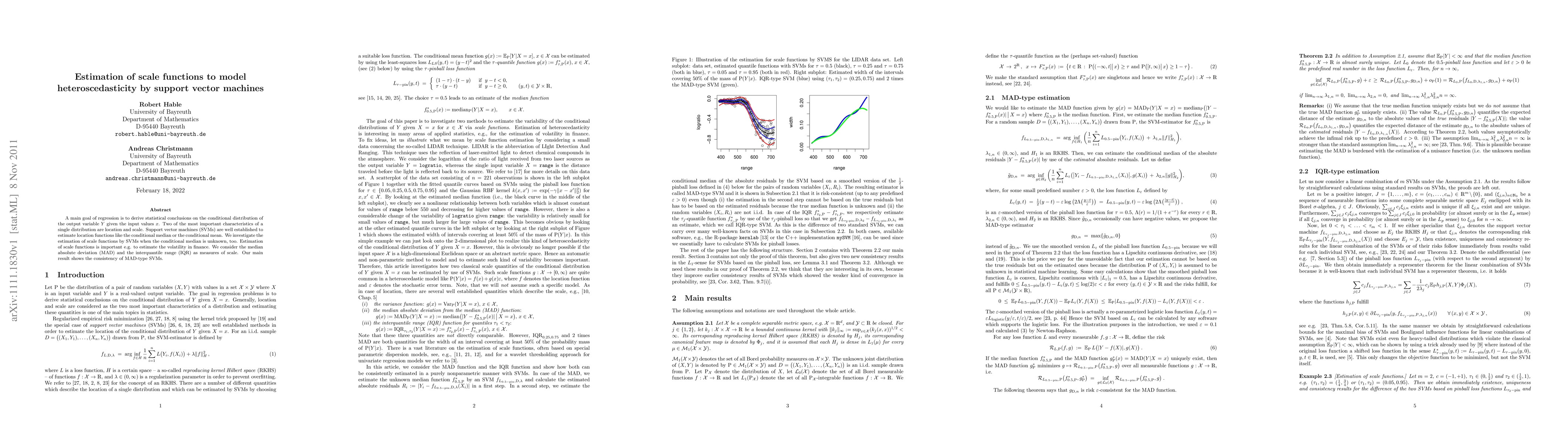

A main goal of regression is to derive statistical conclusions on the conditional distribution of the output variable Y given the input values x. Two of the most important characteristics of a single distribution are location and scale. Support vector machines (SVMs) are well established to estimate location functions like the conditional median or the conditional mean. We investigate the estimation of scale functions by SVMs when the conditional median is unknown, too. Estimation of scale functions is important e.g. to estimate the volatility in finance. We consider the median absolute deviation (MAD) and the interquantile range (IQR) as measures of scale. Our main result shows the consistency of MAD-type SVMs.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0