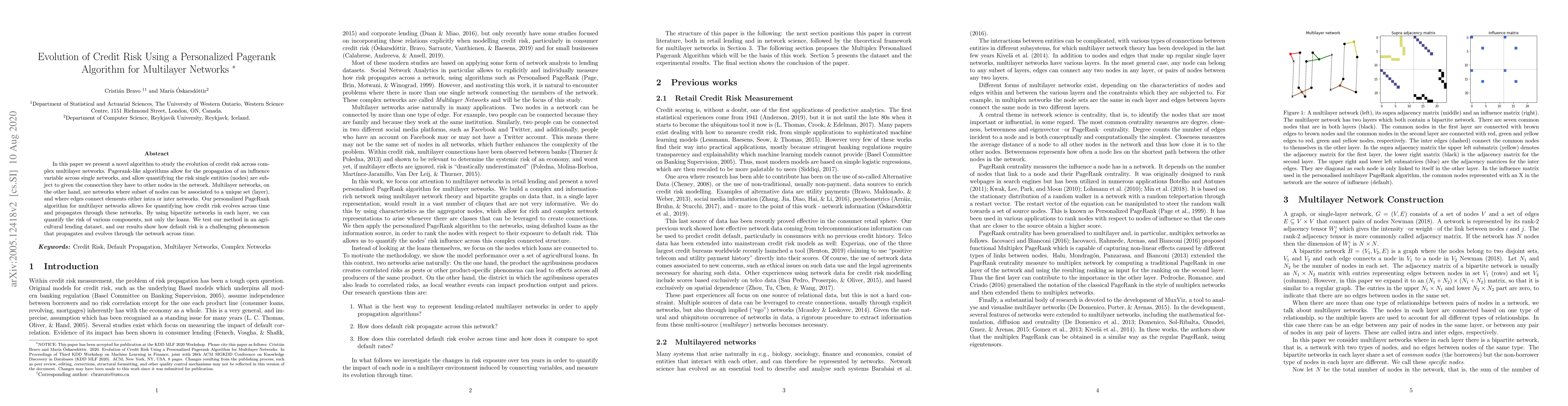

Evolution of Credit Risk Using a Personalized Pagerank Algorithm for Multilayer Networks

Publication

Metrics

AI Quick Summary

This paper introduces a novel personalized PageRank algorithm for multilayer networks to study the evolution of credit risk. The algorithm quantifies how risk propagates across time and through different layers, demonstrating its effectiveness in an agricultural lending dataset.

Paper Preview

Abstract

In this paper we present a novel algorithm to study the evolution of credit risk across complex multilayer networks. Pagerank-like algorithms allow for the propagation of an influence variable across single networks, and allow quantifying the risk single entities (nodes) are subject to given the connection they have to other nodes in the network. Multilayer networks, on the other hand, are networks where subset of nodes can be associated to a unique set (layer), and where edges connect elements either intra or inter networks. Our personalized PageRank algorithm for multilayer networks allows for quantifying how credit risk evolves across time and propagates through these networks. By using bipartite networks in each layer, we can quantify the risk of various components, not only the loans. We test our method in an agricultural lending dataset, and our results show how default risk is a challenging phenomenon that propagates and evolves through the network across time.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0