01

MethodologyHow they did it

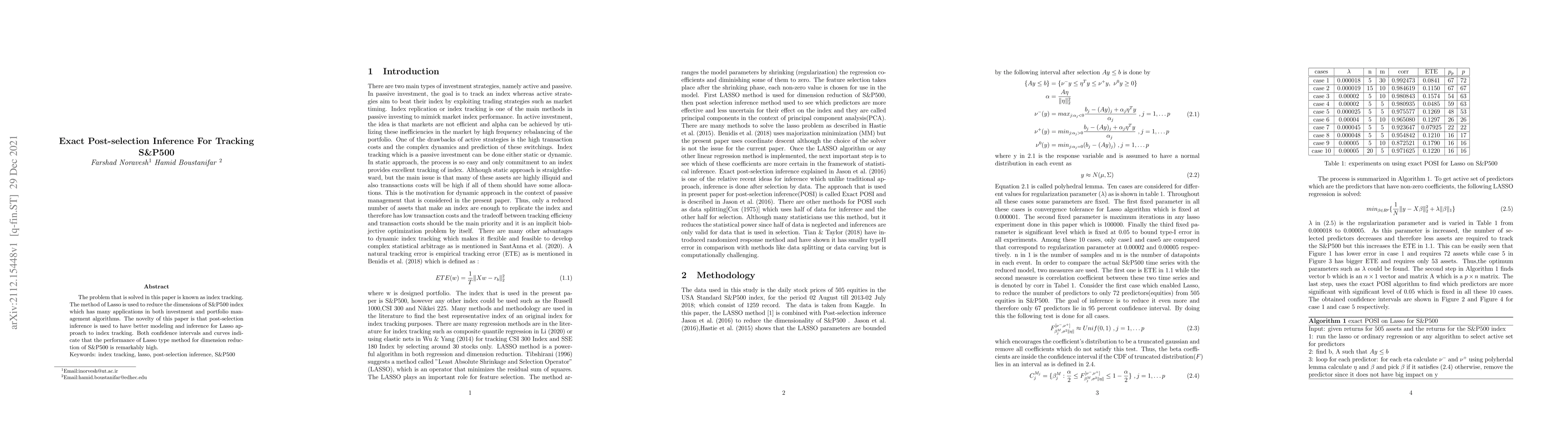

The study uses daily stock prices of 505 equities in the US Standard & Poor's 500 (S&P500) index from August 2, 2013, to July 2, 2018, for dimension reduction. The Lasso method is combined with Post-selection Inference (POSI) to reduce the number of predictors in tracking S&P500. The ExactPOSI algorithm is employed to identify significant predictors with a significance level of 0.05.

Discussion 0