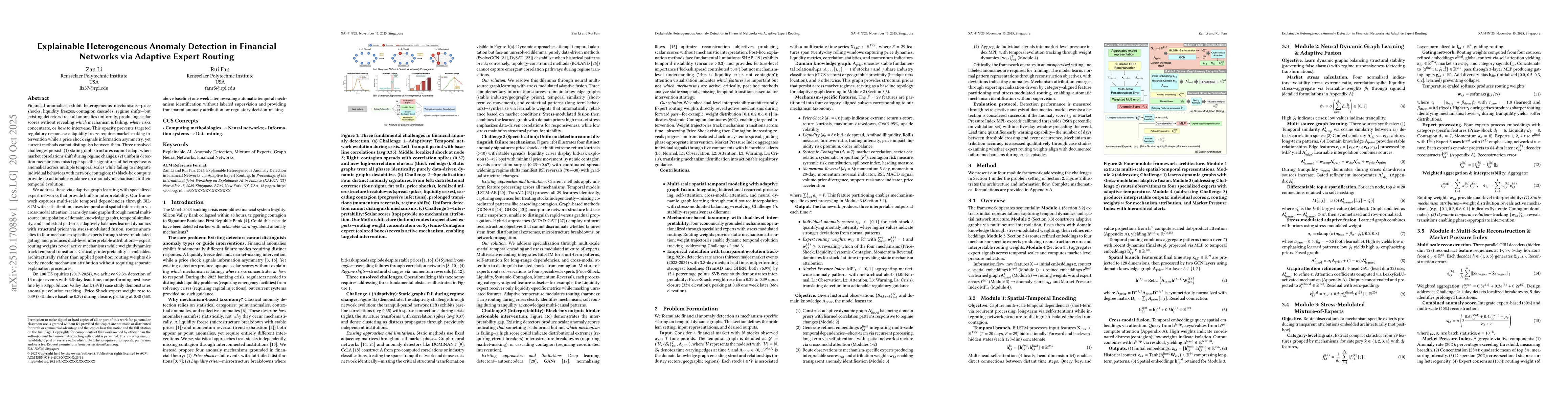

Financial anomalies exhibit heterogeneous mechanisms (price shocks, liquidity

freezes, contagion cascades, regime shifts), but existing detectors treat all

anomalies uniformly, producing scalar scores without revealing which mechanism

is failing, where risks concentrate, or how to intervene. This opacity prevents

targeted regulatory responses. Three unsolved challenges persist: (1) static

graph structures cannot adapt when market correlations shift during regime

changes; (2) uniform detection mechanisms miss type-specific signatures across

multiple temporal scales while failing to integrate individual behaviors with

network contagion; (3) black-box outputs provide no actionable guidance on

anomaly mechanisms or their temporal evolution.

We address these via adaptive graph learning with specialized expert networks

that provide built-in interpretability. Our framework captures multi-scale

temporal dependencies through BiLSTM with self-attention, fuses temporal and

spatial information via cross-modal attention, learns dynamic graphs through

neural multi-source interpolation, adaptively balances learned dynamics with

structural priors via stress-modulated fusion, routes anomalies to four

mechanism-specific experts, and produces dual-level interpretable attributions.

Critically, interpretability is embedded architecturally rather than applied

post-hoc.

On 100 US equities (2017-2024), we achieve 92.3% detection of 13 major events

with 3.8-day lead time, outperforming best baseline by 30.8pp. Silicon Valley

Bank case study demonstrates anomaly evolution tracking: Price-Shock expert

weight rose to 0.39 (33% above baseline 0.29) during closure, peaking at 0.48

(66% above baseline) one week later, revealing automatic temporal mechanism

identification without labeled supervision.

Discussion 0