Explainable Prediction of Economic Time Series Using IMFs and Neural Networks

Publication

Metrics

Paper Preview

Abstract

This study investigates the contribution of Intrinsic Mode Functions (IMFs) derived from economic time series to the predictive performance of neural network models, specifically Multilayer Perceptrons (MLP) and Long Short-Term Memory (LSTM) networks. To enhance interpretability, DeepSHAP is applied, which estimates the marginal contribution of each IMF while keeping the rest of the series intact. Results show that the last IMFs, representing long-term trends, are generally the most influential according to DeepSHAP, whereas high-frequency IMFs contribute less and may even introduce noise, as evidenced by improved metrics upon their removal. Differences between MLP and LSTM highlight the effect of model architecture on feature relevance distribution, with LSTM allocating importance more evenly across IMFs.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

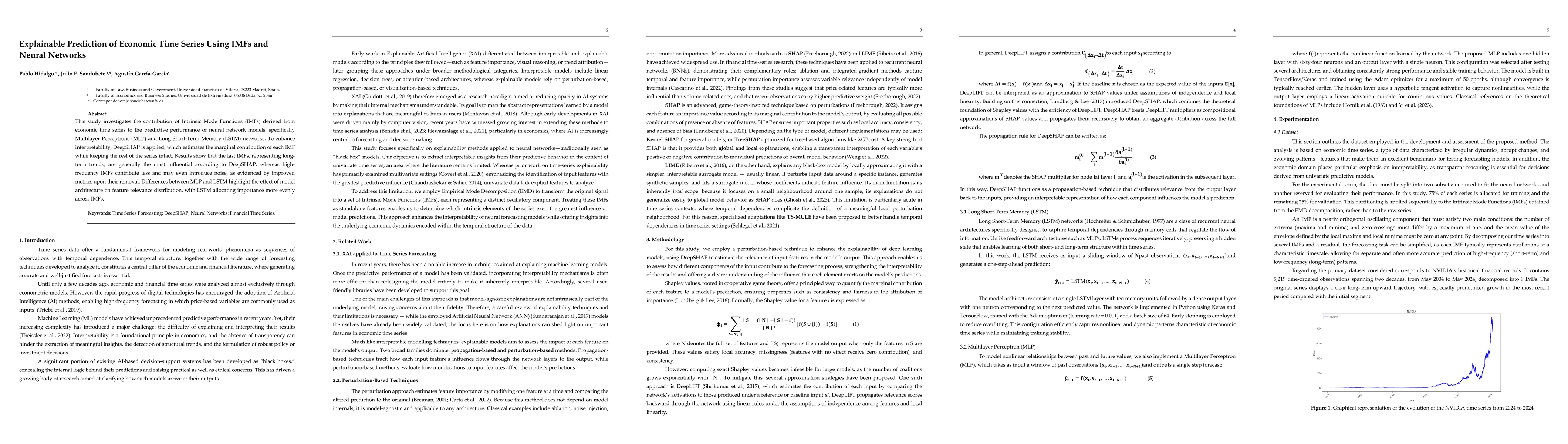

Discussion 0