Extreme value analysis for mixture models with heavy-tailed impurity

Publication

Metrics

AI Quick Summary

This paper explores extreme value analysis in mixture models with heavy-tailed impurity, demonstrating a broader range of possible limit distributions compared to classical theorems. It also showcases the model's effectiveness in analyzing maximal stock returns.

Paper Preview

Abstract

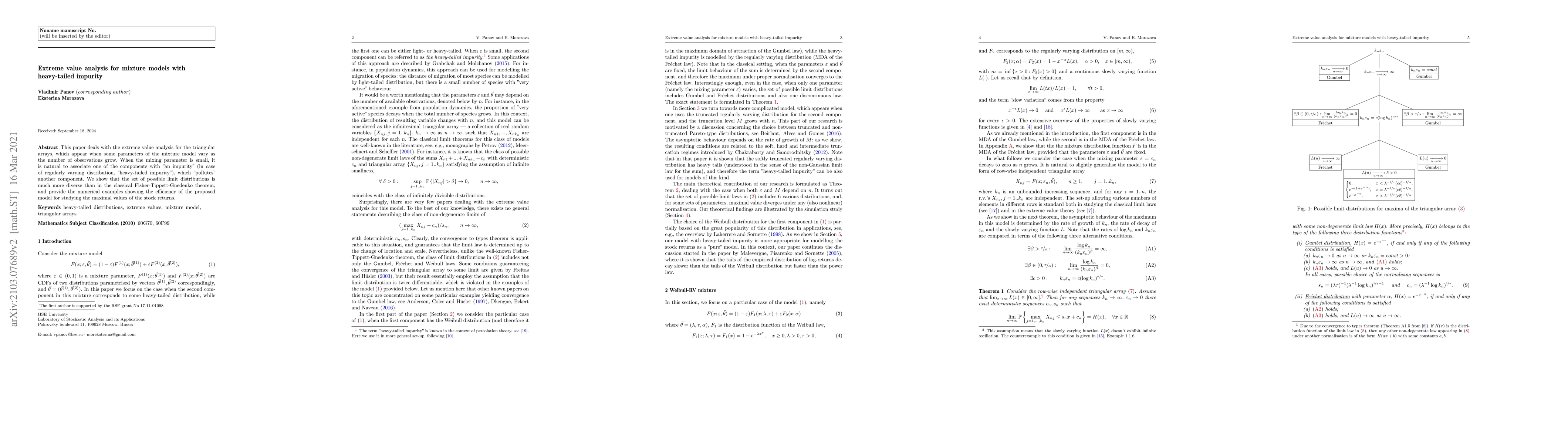

This paper deals with the extreme value analysis for the triangular arrays, which appear when some parameters of the mixture model vary as the number of observations grow. When the mixing parameter is small, it is natural to associate one of the components with "an impurity" (in case of regularly varying distribution, "heavy-tailed impurity"), which "pollutes" another component. We show that the set of possible limit distributions is much more diverse than in the classical Fisher-Tippett-Gnedenko theorem, and provide the numerical examples showing the efficiency of the proposed model for studying the maximal values of the stock returns.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0