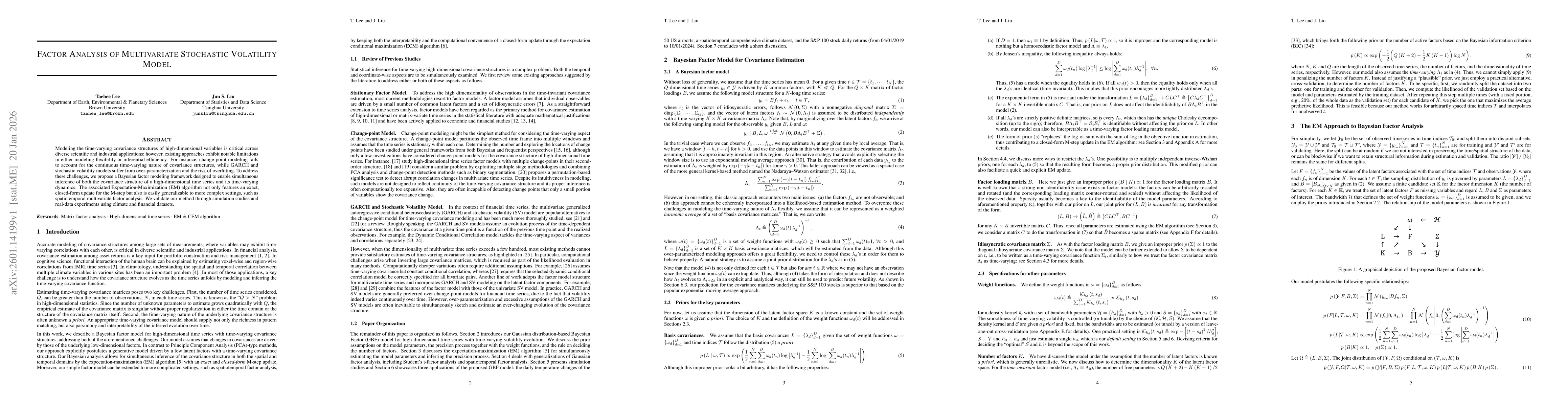

Modeling the time-varying covariance structures of high-dimensional variables is critical across diverse scientific and industrial applications; however, existing approaches exhibit notable limitations in either modeling flexibility or inferential efficiency. For instance, change-point modeling fails to account for the continuous time-varying nature of covariance structures, while GARCH and stochastic volatility models suffer from over-parameterization and the risk of overfitting. To address these challenges, we propose a Bayesian factor modeling framework designed to enable simultaneous inference of both the covariance structure of a high-dimensional time series and its time-varying dynamics. The associated Expectation-Maximization (EM) algorithm not only features an exact, closed-form update for the M-step but also is easily generalizable to more complex settings, such as spatiotemporal multivariate factor analysis. We validate our method through simulation studies and real-data experiments using climate and financial datasets.

Discussion 0