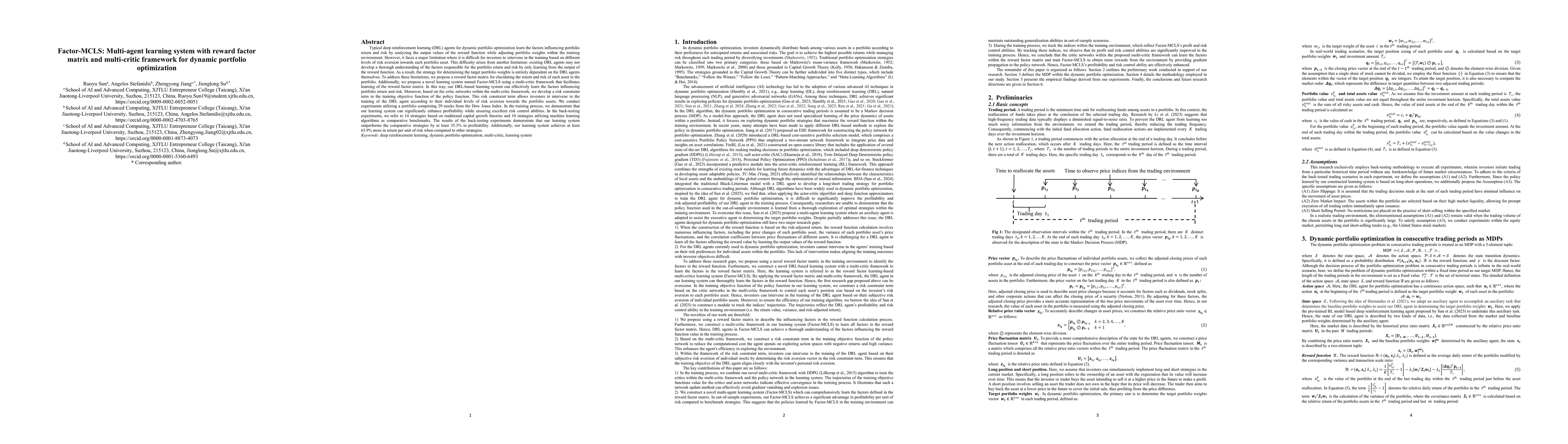

Typical deep reinforcement learning (DRL) agents for dynamic portfolio

optimization learn the factors influencing portfolio return and risk by

analyzing the output values of the reward function while adjusting portfolio

weights within the training environment. However, it faces a major limitation

where it is difficult for investors to intervene in the training based on

different levels of risk aversion towards each portfolio asset. This difficulty

arises from another limitation: existing DRL agents may not develop a thorough

understanding of the factors responsible for the portfolio return and risk by

only learning from the output of the reward function. As a result, the strategy

for determining the target portfolio weights is entirely dependent on the DRL

agents themselves. To address these limitations, we propose a reward factor

matrix for elucidating the return and risk of each asset in the portfolio.

Additionally, we propose a novel learning system named Factor-MCLS using a

multi-critic framework that facilitates learning of the reward factor matrix.

In this way, our DRL-based learning system can effectively learn the factors

influencing portfolio return and risk. Moreover, based on the critic networks

within the multi-critic framework, we develop a risk constraint term in the

training objective function of the policy function. This risk constraint term

allows investors to intervene in the training of the DRL agent according to

their individual levels of risk aversion towards the portfolio assets.

Discussion 0