FactorMiner: A Self-Evolving Agent with Skills and Experience Memory for Financial Alpha Discovery

Publication

Metrics

Paper Preview

Abstract

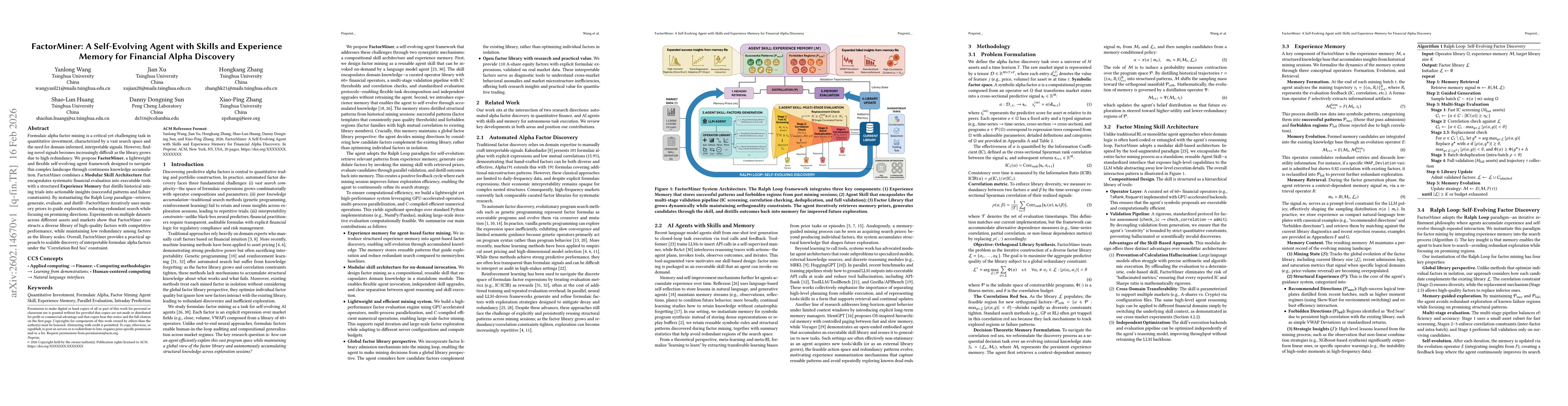

Formulaic alpha factor mining is a critical yet challenging task in quantitative investment, characterized by a vast search space and the need for domain-informed, interpretable signals. However, finding novel signals becomes increasingly difficult as the library grows due to high redundancy. We propose FactorMiner, a lightweight and flexible self-evolving agent framework designed to navigate this complex landscape through continuous knowledge accumulation. FactorMiner combines a Modular Skill Architecture that encapsulates systematic financial evaluation into executable tools with a structured Experience Memory that distills historical mining trials into actionable insights (successful patterns and failure constraints). By instantiating the Ralph Loop paradigm -- retrieve, generate, evaluate, and distill -- FactorMiner iteratively uses memory priors to guide exploration, reducing redundant search while focusing on promising directions. Experiments on multiple datasets across different assets and Markets show that FactorMiner constructs a diverse library of high-quality factors with competitive performance, while maintaining low redundancy among factors as the library scales. Overall, FactorMiner provides a practical approach to scalable discovery of interpretable formulaic alpha factors under the "Correlation Red Sea" constraint.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0