FarmTest: Factor-Adjusted Robust Multiple Testing with Approximate False Discovery Control

Publication

Metrics

AI Quick Summary

This paper introduces FarmTest, a Factor-Adjusted Robust Multiple Testing procedure for controlling the false discovery proportion in large-scale correlated and heavy-tailed data. The method addresses the limitations of conventional methods by incorporating robust factor adjustments, leading to consistent FDP estimation and improved power.

Paper Preview

Abstract

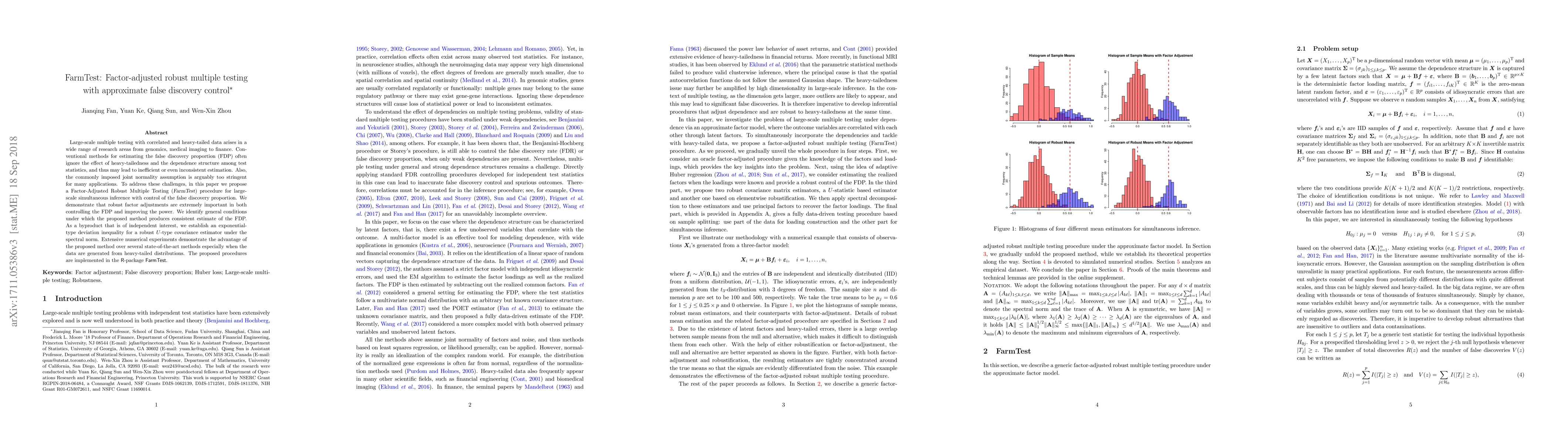

Large-scale multiple testing with correlated and heavy-tailed data arises in a wide range of research areas from genomics, medical imaging to finance. Conventional methods for estimating the false discovery proportion (FDP) often ignore the effect of heavy-tailedness and the dependence structure among test statistics, and thus may lead to inefficient or even inconsistent estimation. Also, the commonly imposed joint normality assumption is arguably too stringent for many applications. To address these challenges, in this paper we propose a Factor-Adjusted Robust Multiple Testing (FarmTest) procedure for large-scale simultaneous inference with control of the false discovery proportion. We demonstrate that robust factor adjustments are extremely important in both controlling the FDP and improving the power. We identify general conditions under which the proposed method produces consistent estimate of the FDP. As a byproduct that is of independent interest, we establish an exponential-type deviation inequality for a robust $U$-type covariance estimator under the spectral norm. Extensive numerical experiments demonstrate the advantage of the proposed method over several state-of-the-art methods especially when the data are generated from heavy-tailed distributions. The proposed procedures are implemented in the R-package FarmTest.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0