Authors

Summary

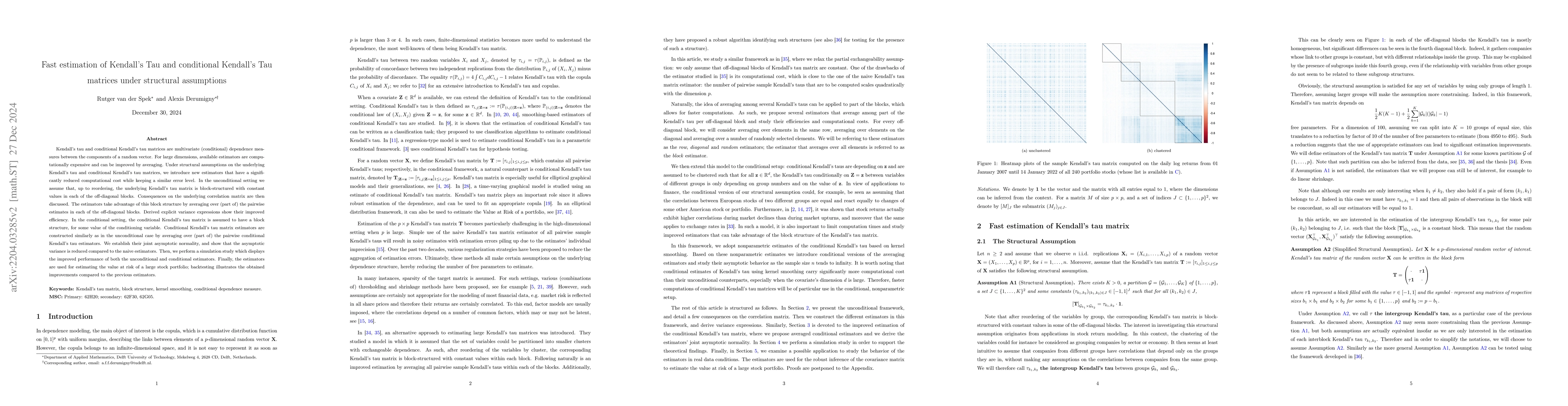

Kendall's tau and conditional Kendall's tau matrices are multivariate (conditional) dependence measures between the components of a random vector. For large dimensions, available estimators are computationally expensive and can be improved by averaging. Under structural assumptions on the underlying Kendall's tau and conditional Kendall's tau matrices, we introduce new estimators that have a significantly reduced computational cost while keeping a similar error level. In the unconditional setting we assume that, up to reordering, the underlying Kendall's tau matrix is block-structured with constant values in each of the off-diagonal blocks. Consequences on the underlying correlation matrix are then discussed. The estimators take advantage of this block structure by averaging over (part of) the pairwise estimates in each of the off-diagonal blocks. Derived explicit variance expressions show their improved efficiency. In the conditional setting, the conditional Kendall's tau matrix is assumed to have a constant block structure, independently of the conditioning variable. Conditional Kendall's tau matrix estimators are constructed similarly as in the unconditional case by averaging over (part of) the pairwise conditional Kendall's tau estimators. We establish their joint asymptotic normality, and show that the asymptotic variance is reduced compared to the naive estimators. Then, we perform a simulation study which displays the improved performance of both the unconditional and conditional estimators. Finally, the estimators are used for estimating the value at risk of a large stock portfolio; backtesting illustrates the obtained improvements compared to the previous estimators.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersOn attainability of Kendall's tau matrices and concordance signatures

Johanna G. Neslehova, Alexander J. McNeil, Andrew D. Smith

| Title | Authors | Year | Actions |

|---|

Comments (0)