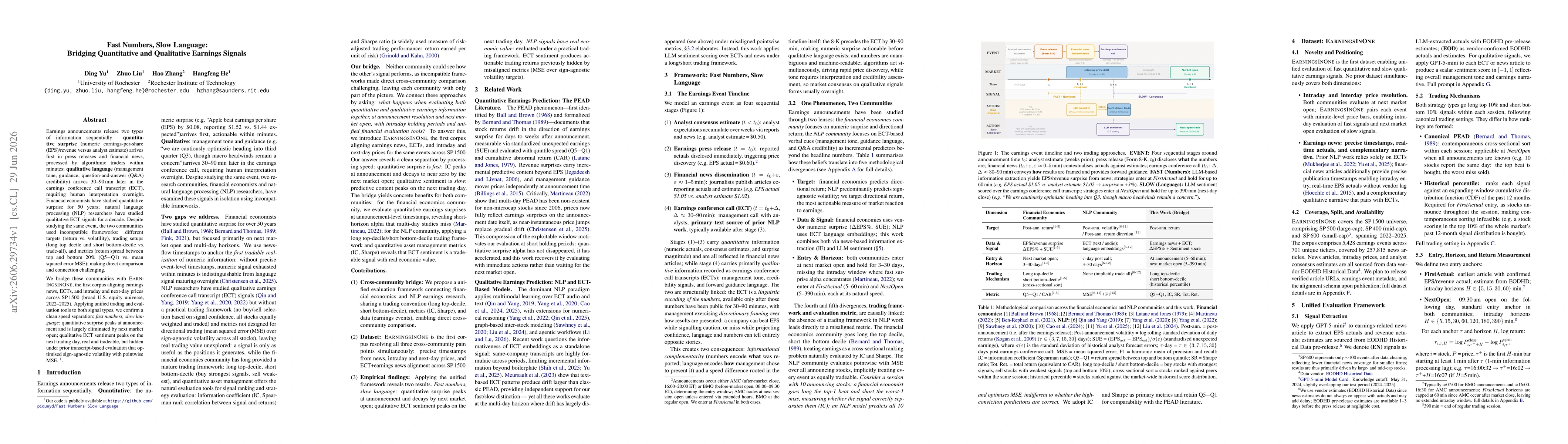

Earnings announcements release two types of information sequentially: quantitative surprise (numeric earnings-per-share (EPS)/revenue versus analyst estimate) arrives first in press releases and financial news, processed by algorithmic traders within minutes; qualitative language (management tone, guidance, question-and-answer (Q&A) credibility) arrives 30-90 min later in the earnings conference call transcript (ECT), requiring human interpretation overnight. Financial economists have studied quantitative surprise for 50 years; natural language processing (NLP) researchers have studied qualitative ECT signals for a decade. Despite studying the same event, the two communities used incompatible frameworks: different targets (return vs. volatility), trading setups (long top-decile and short bottom-decile vs. trade-all), and metrics (return spread between top and bottom 20% (Q5-Q1) vs. mean squared error (MSE)), making direct comparison and connection challenging.

We bridge these communities with EarningsInOne, the first corpus aligning earnings news, ECTs, and intraday and next-day prices across SP 1500 (broad U.S. equity universe, 2022-2025). Applying unified trading and evaluation tools to both signal types, we confirm a clean speed separation, fast numbers, slow language: quantitative surprise peaks at announcement and is largely eliminated by the next market open; qualitative ECT sentiment peaks on the next trading day, real and tradeable, but hidden under prior transcript-based evaluation that optimised sign-agnostic volatility with pointwise MSE.

Discussion 0